India’s rice exports surged by 85.7% year-on-year in October 2024, reversing earlier declines seen in FY24. This turnaround was driven by the removal of export bans and duties, alongside a record Kharif crop production estimate of 119.93 million tonnes (Jun-Nov, 2024). Indian exporters faced challenges in 2023 due to regulatory measures aimed at stabilizing domestic prices, which disrupted global markets and pushed rice prices to an 11-year high.

The easing of restrictions in September, coupled with renewed demand from countries like Indonesia and Mauritius, has revitalized exports. With competitive pricing and government support, India is poised to expand its market share, potentially exporting an additional 10 million metric tons by March 2025. This shift has also contributed to a decline in global rice prices, particularly in Asia, stabilizing markets after a volatile year.

India’s rice exports witnessed a YoY growth of 85.7% in October, an extraordinary surge compared to the declining trend seen in earlier months of FY ’24. Before understanding the reasons behind this shift, it is helpful to first explore the dynamics of the global rice market and India’s role within it.

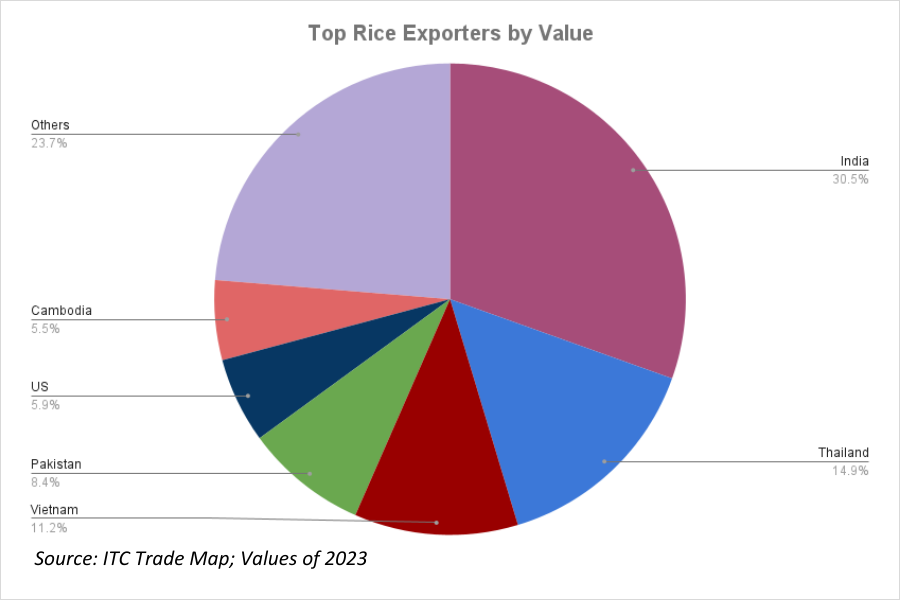

Indian rice is globally valued for its aroma, texture, and versatility, though it has faced challenges in recent years, including exclusion from tenders by key importing nations. When it comes to production, China leads as the largest producer of rice, with India following as the second-largest followed by Vietnam as the third. However, in exports, China significantly lags, ranking as the 7th largest exporter.

India accounted for 30.5% of the total rice traded globally in 2023. Together, the top three rice-exporting nations—India, Thailand, and Vietnam—contribute to more than half of the world’s rice exports. Other notable exporters include Pakistan, the US, Cambodia, and China.

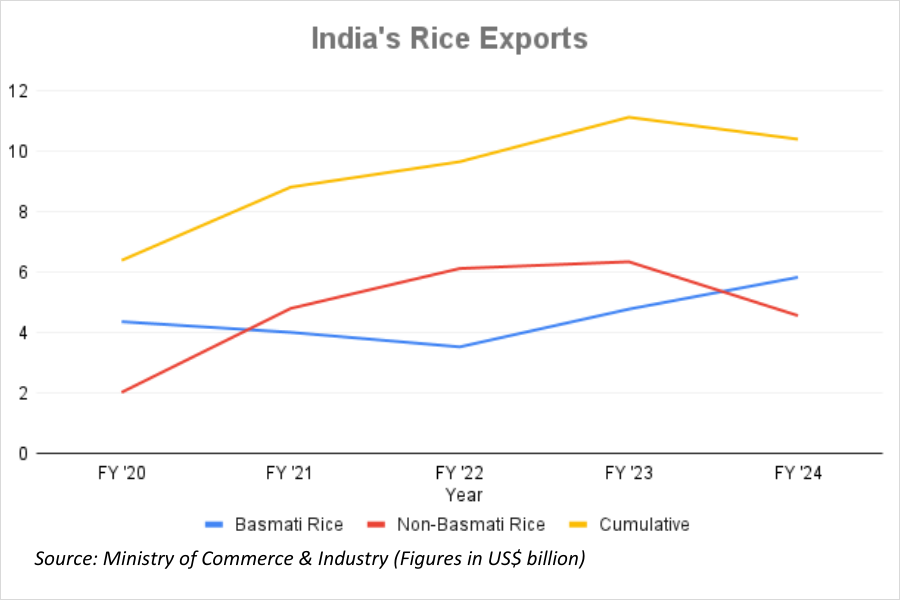

In FY20, exports of Basmati rice surpassed those of non-Basmati rice. However, Basmati exports saw a decline until 2022 before beginning to recover. In contrast, non-Basmati rice exports experienced consistent growth until 2023, only to face a sharp decline between 2023 and 2024 due to regulatory changes. Despite these fluctuations, India’s cumulative rice exports showed a 5-year CAGR of 6.1%.

What Changed in 2023?

India’s rice export landscape shifted significantly in 2023 due to regulatory interventions aimed at stabilizing domestic markets. On July 20, 2023, the Government of India implemented an export ban on white non-Basmati rice, immediately halting shipments of semi-milled or whole-milled varieties. This followed a prior measure from September 2022, when a 20% export tariff was introduced on non-Basmati white and brown rice to discourage exports and ensure local availability.

Globally, the impact of India’s restrictions coupled with the already rising international rice prices. According to the FAO, the global rice price index increased by 14% for all rice and 16% for Indica (long-grain) varieties in mid-2023 since June 2022. The global rice prices in 2023 soared to their highest in 11 years.

Further tightening occurred on August 25, 2023, when the government imposed a 20% export duty on parboiled non-Basmati rice, due to rising domestic rice prices. The reason for the shortage was the damage caused by late but heavy monsoon rains & flooding in northern states like Punjab and Haryana, which forced many farmers to replant crops, straining supply chains. Over the year, retail rice prices increased by 11.5%, prompting the government to prioritize domestic price availability. Combined, these factors reshaped both Indian and global rice markets in 2023.

India’s rice export ban in 2023 raised inflation concerns and threatened global food security. This curb affected approximately half of India’s rice exports, with the targeted categories—non-basmati white and broken rice—accounting for 10 million tons out of the 22 million tons of exports in 2022.

Given that rice is a staple for over 3 billion people and nearly 90% of its cultivation occurs in Asia, where El Niño-driven lower rainfall heightens production challenges, the ban exacerbated fears globally. But fortunately, the impact of El Niño in 2023-24 was less severe than initially forecasted. The decision particularly impacted African nations, heavily dependent on Indian rice imports, prompting many to urge New Delhi to reconsider its stance.

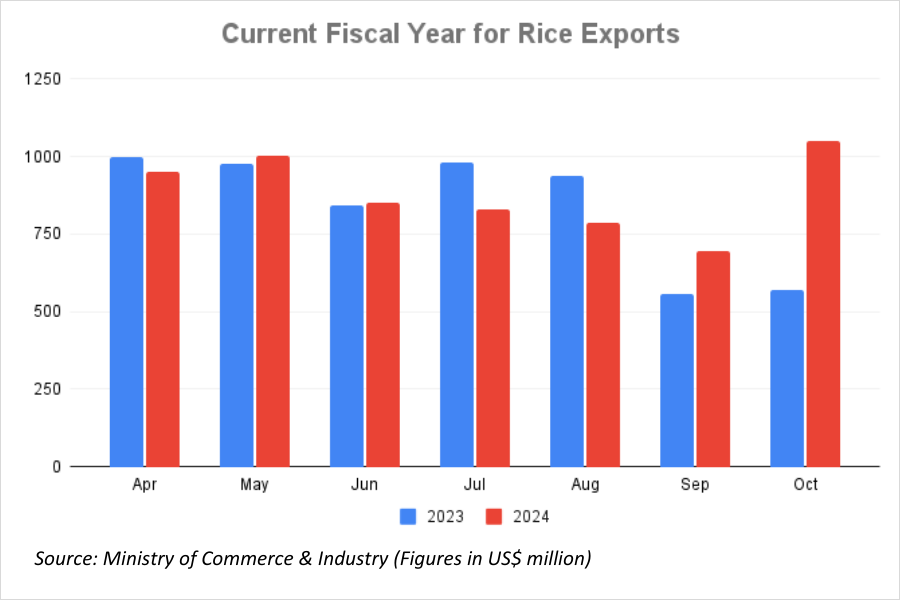

In FY 2024-25, the effects of the ban are visible, with India’s rice exports experiencing flat or negative YoY growth in the initial months, except in May. However, September and October saw dramatic increases of 49.1% and 85.7%, respectively driven by key policy measures.

On September 27, 2024, India removed the 20% export duty on Non-Basmati White Rice. The government also lifted the export ban on this rice and set a minimum export price (MEP) of US$ 490 per tonne. By October 23, the MEP was scrapped, making rice exports more flexible. Additionally, the government reduced export duties on three other rice categories—from 20% to 10%—including husked (brown), parboiled, and paddy rice. By October 22, duties on other rice types were either halved or completely eliminated making Indian rice more competitive in global markets.

These policy shifts aligned with a record Kharif crop production estimate of 119.93 million tonnes for 2024-25, reflecting a 5.8% year-on-year growth. This bumper harvest contributes well to India’s capacity to meet global demand and enhance its competitive edge, particularly against leading exporters like Thailand and Vietnam.

During a recent CNBC Aawaz interview with Dr Prem Garg, president of the India Rice Exporter Federation (IREF), it was discussed that the government had even introduced a 0.9% benefit under the RoDTEP scheme for parboiled rice exports along with a cut on export duties, with expectations of a similar benefit for white rice in the future. The industry is also hopeful for GST-related benefits. In addition, cargo approvals from Indonesia, Bangladesh, and Mauritius in October have opened up fresh export opportunities for India. With these changes, India’s rice exports could potentially increase by 10 million metric tons, though a more realistic estimate is around 6 million metric tons by March 2025 as discussed in the interview.

Influence on global rice prices

The IMF had advocated India lift its rice export bans to address global supply shortages and help the decade-high surge in prices. Since late September, when India began easing its export restrictions, rice prices in Asia have started to decline, depite strong demand from countries like Indonesia and the Philippines. For example, the price of Thai 5% broken rice fell below US$ 500 per metric ton in mid-October, the lowest since July 2023. Similarly, Pakistani 5% broken rice saw a sharper price drop as it directly competes with Indian rice in key African markets. According to the November 6th Creed Rice Market Report, India’s non-basmati white 5% rice is now priced at around US$ 465 per metric ton, undercutting competitors. However, rice remains expensive in western countries, as the recent price drops haven’t fully reached these markets yet.

“The recent surge in exports can largely be attributed to the opening up of India’s non-basmati rice markets. Currently, Indian prices are highly competitive in comparison to global prices, which has bolstered demand for Indian rice. However, as global markets adjust, prices will likely align and eventually soften,” said Vijay Agarwal, Director of Bharat International Pvt Ltd.

Since India rolled back its restrictions, global rice prices have quickly returned to pre-restriction levels. As India’s exports continue to grow and strengthen, more the integration between the markets. And as we achieve higher integration, further price drops and more stable rice markets worldwide can be expected.

Conclusion

The outlook for the rice export market is indeed positive. But domestic availability remains a critical concern, particularly given India’s reliance on rice as a staple food. The previous ban was prompted by crop failure and soaring domestic prices. While it temporarily stabilized local markets, it also disrupted global trade. Should such a ban be imposed again, and how can India mitigate the need for such drastic measures in the future?

Devinder Sharma, Food and Agricultural Policy Expert, Researcher, and Writer, explains, “Domestic availability of rice will not be affected, as we are only exporting surplus, and it’s in our best interest to keep the export channels open. However, in times of crisis, any government would be justified in deciding to impose bans if necessary. The only thing we can do is help mitigate any expected shortfall in rice production by providing necessary support.”

To avoid such bans, India needs to undertake strong measures to support its farmers by ensuring adequate crops are grown locally and addressing preventable crop failures. For example, Uttar Pradesh, India’s largest farming state with 237 million people, faces serious risks from climate change, which is expected to reduce rice production. While more rainfall might help rainfed rice in dry areas, it could also lower the need for irrigation. Planting earlier in the season could help reduce losses for irrigated crops, but the overall impact of climate change on rice yields is worrying and threatens food security.

To address this issue, a long-term plan is essential, including strategies to combat climate change, training programs and modern techniques to help farmers adapt. These efforts should focus on promoting climate-resilient crop varieties, improving water management practices, and helping farmers cope with changing weather patterns. Additionally, support systems such as accessible credit, insurance schemes, and market linkages can further strengthen their resilience and ensure sustainable growth.