India’s tech startup ecosystem

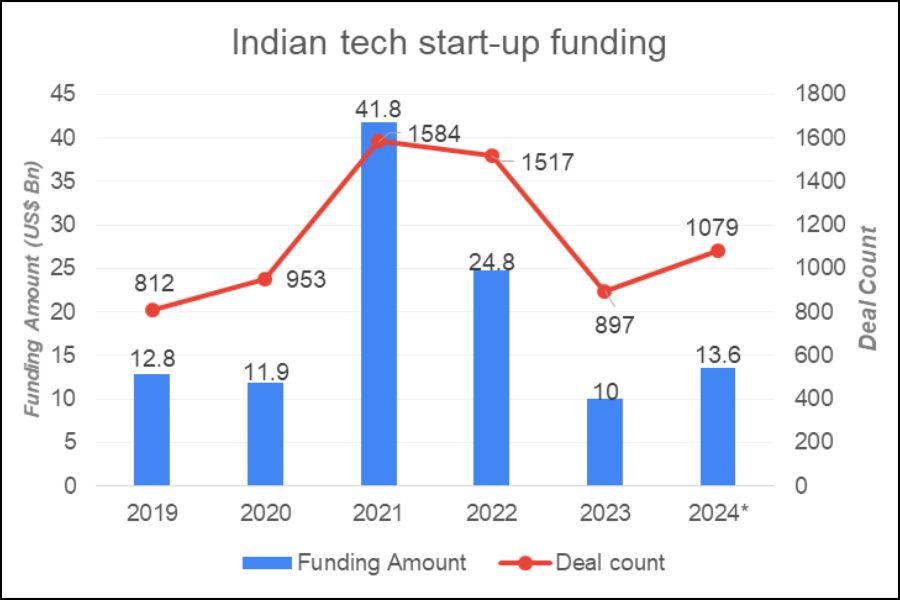

The Nasscom and Zinnov report on the Indian Tech Startups for 2023 confirmed India’s position as the third-largest tech startup ecosystem globally, with over 950 tech startups established in 2023, contributing to more than 31,000 tech startups in the past decade. The cumulative funding for these tech startups from 2019 to 2023 exceeds US$ 70 billion, demonstrating robust growth and investment in the Indian tech startups.

Source: Nasscom

The report highlighted that better Internet connectivity, digitalization, and government-led initiatives have significantly supported startups. Key sectors receiving maximum funding from 2014 to 2023 include retail, enterprise applications, fintech, transportation and logistics technology, food and agriculture tech, auto technology, travel and hospitality tech, and edtech.

Despite global challenges like valuation issues, less IPOs , regulatory changes, and macroeconomic and geopolitical trends in 2023, Indian tech startups remain focused on improving business fundamentals, profitability, and revenue streams. The Nasscom-Zinnov Tech Startup Survey-2023 found that about 60% of startup founders saw increased revenue and profitability by 2023.

Unfunded tech startup founders also anticipated higher revenues in 2024 compared to their funded peers. The report highlighted the growing use of DeepTech, with startups leveraging it to improve efficiency (59%), reduce costs (52%), and automate operations (41%).

The study noted the democratisation of tech in 2023, leading startups to diversify into Tier 2 and Tier 3 cities, with 40% of tech startups established in emerging hubs by 2023. According to Nasscom, business model innovations in industries like manufacturing, automotive, and industrial sectors improved over the past year, with these sectors seeing increased stability and funding.

Debjani Ghosh, President of Nasscom, said, “In 2023, despite facing global economic and regulatory challenges, Indian tech startups have prioritised the imperative of enhancing their business fundamentals, driving profitability, and growth. India’s tech startup ecosystem has truly matured, attracting more than US$ 70 billion in cumulative funding between 2019 to 2023.”

Funding scenario in tech startups

Indian tech startups raised US$ 4.1 billion in H1 2024, 4% higher than H2 2023 (US$ 3.96 billion), remaining the fourth-highest funded country globally in the tech startup, according to Tracxn report that highlighted funding trends and volumes in the Indian tech startup landscape.

*Calculated based on the average annual growth rate of funding amount between 2014 to 2023

Source: Inc42 and Nasscom

Startup funding in India has been declining since 2021, as central banks increased interest rates, ending the era of cheap money from the Covid-led low interest rate regime. Risk-capital investors pulled back on venture funding.

According to the report, seed stage funding rose to US$ 455 million, a 17.3% decrease from H1 2023 but a 6.5% increase from H2 2023. Early stage startups maintained a valuation of US$ 1.3 billion, 28% less than H1 2023 but consistent with H2 2023. Late-stage funding decreased by 1.3% from H1 2023 to US$ 2.4 billion but rose by 3.8% from H2 2023.

Despite these challenges, eight funding rounds over US$ 100 million were completed in H1 2024, including Meesho’s US$ 275 million Series F round, Flipkart’s US$ 350 million Series J round led by Google, and Apollo 24|7’s US $ 297 million PE round.

Neha Singh, Co-Founder of Tracxn, noted that despite four consecutive half-year periods of declining funding since H1 2022, signs of stabilization and growth are emerging. “India’s robust performance as the fourth-highest-funded country in the tech startup ecosystem is encouraging.”

Three unicorns emerged in H1 2024, up from zero in H1 2023, along with 33 new “Soonicorns“—startups expected to become unicorns soon. H1 2024 saw 17 IPOs, up from 6 in H1 2023 and 12 in H2 2023.

Acquisitions in the Indian startup ecosystem fell from 75 in H1 2023 to 43 in H1 2024. Notable acquisitions included PingSafe by SentinelOne for $100 million and PureSoftware by Happiest Minds for US$ 94.5 million.

Accel, Blume Ventures, and Peak XV Partners were the top investors in H1 2024. In the seed stage, Venture Catalyst, Z Nation Lab, and We Founder Circle led. Peak XV Partners, Global Alpha Waves, and Saama Capital were the most active early-stage investors. DST Global, Epiq Capital Advisors, and the UC-RNT Fund led late-stage investments.

Significant funding rounds included Capillary Technologies’ US$ 95 million in February, a $90 million round for a lending platform in June, and Perfios’ US$ 80 million round from the Ontario Teachers’ Pension Plan in March.

Challenges startups are facing

Indian startups encounter difficulties securing adequate funding for their ventures. Limited access to capital inhibits growth potential and hampers innovation. Startups face challenges in attracting investors and obtaining venture capital due to various factors, such as risk aversion, uncertain market conditions, and a lack of investor confidence. The other challenges are as follows:

- Revenue Generation: Many startups face challenges in generating sustainable revenues. They often struggle to find viable business models, monetize their products or services, and achieve profitability.

- Lack of Supportive Infrastructure: The absence of a robust infrastructure ecosystem can impede the growth of start-ups. Challenges include inadequate physical infrastructure, limited access to technological resources, and a dearth of incubation centres, mentorship programmes, and networking opportunities.

- Regulatory Environment and Tax Structures: Startups in India face regulatory hurdles and complex tax structures, and seek simplification in these areas.

“Startups have several expectations from the upcoming budget to alleviate challenges. Primarily, I hope for the provision of additional funds specifically aimed at MSMEs to ensure easier access to bootstrap funding for early-stage startups. Policy reforms are also anticipated to facilitate better working capital management and ensure the efficient disbursement of funds. Moreover, there is an expectation for public sector companies to be mandated to lend a certain amount of funds to startups, with streamlined processes to make securing loans easier,” said Avdhesh Dwivedi, founder and CEO of FifthGen Tech Solutions.

He further adds, that simplifying compliance requirements would also help reduce the burden on startups, allowing them to focus more on their core business activities. Enhanced support systems, especially for startups in sectors like pharmaceuticals and IT, are also expected to be part of the budget measures.

In 2024, technology, particularly in manufacturing and hardware, could catalyze a rebound despite current high valuations. AI’s strategic integration promises substantial growth across industries, emphasizing value creation over mere scaling for IP-driven startups. While some sectors like AI, fintech, enterprise software, healthtech, and sustainability tech may see increased investor interest by late 2024, direct-to-consumer brands could face funding challenges due to market saturation.

Despite favorable factors like easing inflation and reduced currency challenges, the startup landscape might not fully recover in 2024 as far as new ventures are concerned. Investors are now looking for more profitable long term businesses to invest rather then new ideas to mitigate risks.With approximately US$ 20 billion ready for deployment, investors will likely prioritize sustainable innovations and proven profitability in their funding decisions.