The global drive to decarbonize transportation has placed biodiesel at the center of clean-fuel strategies. It promises lower emissions and easy integration with existing engines, but rapid biodiesel expansion has triggered difficult questions around food security, land pressure, subsidies, and environmental risk. When edible oils power vehicles as well as kitchens, energy policy becomes a delicate balancing act.

Indonesia’s shift toward higher palm oil–based blends, now moving from B40 to B50, is the most significant real-world test of this challenge. The program has improved energy self-sufficiency, yet has also tightened edible oil supplies, increased fiscal burdens, and amplified concerns about deforestation and climate-driven yield volatility.

For India, which imports most of its edible oils while advancing its own biofuel mandate, Indonesia’s experience is both a warning and a guide. This article examines the global context, Indonesia’s approach, and the key lessons India must adopt to ensure clean energy progress does not compromise food and economic security.

The rising global demand for cleaner and more sustainable fuels is accelerating the shift toward biofuels over the past few years. Broadly, biofuels are renewable fuels derived from biomass and are being increasingly adopted as a key measure to curb carbon emissions, combat climate change, and enhance energy security. They are primarily produced in two forms—ethanol and biodiesel. While ethanol is made from sugar- and starch-rich crops like cereals, biodiesel is produced mainly from oilseed crops such as palm, rapeseed, sunflower, and soybean.

Biodiesel’s ability to ensure complete combustion significantly reduces greenhouse gas (GHG) emissions, making it a preferred alternative to fossil fuels. High compatibility with existing diesel engines further strengthens its appeal, while expanding vehicle ownership and industrial applications continue to drive consumption worldwide. It is gaining traction in the automotive sector for its lower emission profile. Emerging economies such as India, China, Brazil, and several EU nations have also announced targets to substitute 10–20% of fossil-based fuels in transportation with biodiesel. As nations pursue decarbonization goals, the challenge lies in advancing biodiesel growth without compromising global food security.

Biodiesel production has been inextricably connected to the “food versus fuel” debate, raising concerns about global food security with the diversion of agricultural land and resources toward its production. As more cropland gets redirected for fuel production, the availability of land for food cultivation shrinks, potentially affecting food supplies and prices. With a growing global population and increasing food demand, balancing energy generation with food production has become essential. Poorly designed incentive structures for biodiesel adoption could unintentionally worsen food insecurity and contribute to price volatility in global food and edible oil markets.

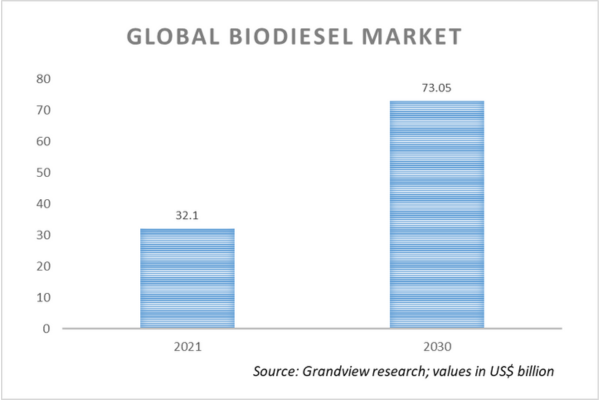

The global biodiesel market, valued at US$ 32.1 billion in 2021, is expected to grow at a CAGR of 10% from 2022 to 2030, reaching an estimated value of US$ 73 billion by the end of the decade. Among the various feedstocks available for biodiesel production, palm oil stands out due to its high oil yield, efficiency, and cost-effectiveness. Mature oil palm plantations can produce around 3 tons of oil per hectare annually—far exceeding the output of other major oilseeds such as soy, rapeseed, and sunflower. This high productivity is particularly valuable in a world where arable land is limited, yet the demand for renewable energy sources continues to grow.

Global production and demand

To promote biodiesel production, many countries have implemented public support policies aimed at developing and sustaining biodiesel markets. This approach comes from the fact that biodiesel production costs remain higher than those of fossil fuels, despite recent improvements in efficiency. One of the most common forms of policy support is the introduction of blending or use mandates, which require a minimum share of biodiesel content in diesel—primarily in the transportation sector, though these requirements are sometimes extended to industrial and agricultural uses as well.

Globally, biodiesel blending mandates vary widely. The United States blends biodiesel at around 2.5%, while Brazil maintains a B10 mandate. In the European Union, biodiesel blending is set at B7, whereas China’s biodiesel admixture remains low at about 0.2% due to limited enforcement. India keeps the target of blending at 5%.

Among the leading biofuel-producing nations, Indonesia stands out for its ambitious blending targets and rapid policy-driven expansion. The country leads globally with the highest mandate at B40, with plans to raise it to B50, which was was successfully implemented by March 2025 after a technical transition period. It’s government has positioned palm oil as a central biofuel feedstock. The program has performed beyond government projections, with demand already exceeding the 2025 target of 15.6 million kiloliters and additional requests for 100,000–200,000 kiloliters expected before the end of the year.

This strong domestic consumption has created a structural tightening in Indonesia’s export supply, carrying significant consequences for global market dynamics. As of 2021, Indonesia and Malaysia together contributed nearly 85% of global palm oil output, with Indonesia alone producing about 50 million metric tons annually (Ritchie, 2022). Industry estimates indicate that achieving a B50 blend would require around 20 million metric tons of biodiesel, demanding roughly 2 million more tons of crude palm oil than current B40 levels.

The economic rationale behind Indonesia’s aggressive biofuel expansion raises several concerns. While the B40 and upcoming B50 programs aim to enhance energy self-sufficiency, their long-term financial sustainability remains uncertain. The government is projected to spend 35.5 trillion Indonesian rupiah (approximately US$ 2.1 billion) on biodiesel subsidies in 2025 alone—nearly double the amount allocated in 2023. If subsidy expenditures begin to exceed tax revenues, Indonesia could face growing fiscal pressure.

Transitioning to higher biodiesel mandates also presents multiple challenges, as reflected in Indonesia’s B50 experience. Below are the challenges which Indonesia faces in transitioning to B50 mandate.

Technical implementation hurdles: Indonesia’s delay in rolling out B50 underscores the technical challenges of adopting higher biodiesel blends. The government has yet to complete road tests and feasibility studies, casting doubt on meeting the initial timeline. Concerns over engine performance, especially in heavy-duty sectors like mining and agriculture, remain key obstacles. Although existing capacity of around 19.6 million kiloliters could support B50, infrastructure and blending logistics pose practical hurdles. As a result, a phased transition, with B45 as an interim step, is being considered to enable further testing and smoother implementation.

Economic feasibility and subsidy requirements: The economic sustainability of Indonesia’s higher biodiesel mandates is increasingly uncertain under current market conditions. The Palm Oil Plantation Fund Management Agency (BPDPKS) is expected to spend Rp 51 trillion (US$ 3.1 billion) on B40 subsidies in 2025, far exceeding the government’s initial estimate of Rp 35.5 trillion. The energy ministry’s request for an additional Rp 16 trillion to cover unpaid 2024 subsidies further underscores the program’s rising fiscal strain.

Learnings for India

India stands at a decisive moment in its clean-energy transition. Biofuels will play a vital role in reducing emissions and enhancing energy security, but Indonesia’s experience shows what happens when the push for greener fuels collides head-on with national food needs and fiscal realities. With high dependence on imported edible oils, India cannot afford to route scarce food resources into fuel production. The country’s biodiesel future must therefore be rooted in non-edible and waste-based feedstocks such as used cooking oil, agri-residues, and algae. Alongside this, robust sustainability norms, transparent traceability systems, and prudent subsidy frameworks are essential to prevent land-use conflicts, price shocks, and environmental damage.