Not long ago, booking a seat to space sounded like something out of The Jetsons. Today, it’s inching closer to reality. Tourists are strapping into rockets, companies are dreaming up orbital hotels, and governments are reshaping laws to let private players join the race. India’s own Space Policy 2023—its “Space Act moment”—has thrown open the gates for startups, investors, and global partners to build alongside ISRO. What was once the playground of astronauts is slowly becoming an adventure people can imagine for themselves. Ten years ago, the idea of booking a ticket to space felt like pure fiction like the Jetsons. Today, it’s edging into reality. Billion-dollar companies are flying passengers beyond Earth, startups are experimenting with new experiences, and governments are rewriting rules to make way for private players. What was once a dream reserved for sci-fi movies—or the ultra-wealthy—is beginning to take shape as a real industry. By 2030, suborbital tourism alone could be worth US$4 billion, and the broader space tourism market may exceed US$10 billion annually. That’s no longer a futuristic daydream—it’s a business plan in motion. Today companies like Blue Origin has restarted its New Shepard launches, sending paying customers on short trips past the edge of space. Virgin Galactic has paused its early flights but is building its next-generation Delta-class spaceplanes, due in 2026. Tickets are steep between US$ 450,000–600,000—but that hasn’t stopped adventurers from signing up. At the other end of the spectrum are orbital missions. Axiom Space, in partnership with SpaceX, successfully launched the first private crew, Ax-1, to the International Space Station (ISS) in April 2022, with each of the four crew members paying approximately US$ 55 million for the mission. The Axiom-1 mission was a historic, fully private, and funded flight to the ISS, utilizing a SpaceX Crew Dragon capsule for transportation and including eight days of research and philanthropic work aboard the station. SpaceX’s Polaris Dawn mission, launched in September 2024, not 2024 successfully conducted the first-ever private spacewalk and reached an altitude of 1408 kms, marking the highest Earth orbit achieved by humans since the Apollo program. During the five-day flight, the crew also studied the effects of radiation and performed various experiments, including testing new spacesuits For those not ready to mortgage a small country, there’s Zero-G’s parabolic flights at around US$ 8,900, giving passengers a few minutes of weightlessness. Balloon-based journeys promised gentle rides to the stratosphere, but the collapse of Space Perspective in 2025 showed how brutally hard the business can be. Where is this headed? Private space stations, such as Axiom Station, Orbital Reef, and Starlab, are in development with plans to host a mix of researchers, corporate clients, and tourists in the late 2020s. These private orbital outposts are being designed to operate concurrently with the International Space Station (ISS) before its planned retirement around 2030, marking a major shift toward a commercialized low-Earth orbit (LEO) economy. At the same time, new vehicles could transform access. Virgin Galactic’s Delta planes promise more frequent flights. SpaceX’s Starship, still in testing, could slash costs by carrying far more passengers and cargo in a single trip. In the mid-term, bundled packages—astronaut training, Zero-G flights, suborbital hops—will make the whole adventure feel more immersive. Long-term? Hotels, residencies, and research hubs in orbit. India’s place in the space story The Indian Space Policy 2023 officially shifts ISRO’s focus from commercial launch operations and manufacturing to pure research, advanced missions, and expanding human space exploration. The policy creates an enabling environment for private companies to enter and participate in all aspects of the space sector. To back this up, the government opened the doors wider for foreign investment in 2024 and even transferred ISRO’s Small Satellite Launch Vehicle (SSLV) technology to Hindustan Aeronautics Ltd (HAL) in 2025. Startups like Skyroot and Agnikul are already building their own rockets, and partnerships with international space station projects don’t seem far off. As the Financial Times noted, India isn’t just a low-cost option anymore—it’s emerging as a serious commercial contender. For tourism, this means India could soon be more than just a launchpad; it could be a partner in shaping the experiences themselves. Private space tourism is still ultra-exclusive, but it’s no longer make-believe. The industry’s future hinges on lowering costs, improving safety, and flying more often. It’s about an entire ecosystem being built to make cosmic travel part of the human journey. Top 5 FAQs on space tourism 1. What types of space tourism trips are currently available?Space tourism comes in two primary forms: suborbital (short flights beyond the edge of space with a few minutes of weightlessness) and orbital (longer missions orbiting the Earth, often aboard spacecraft like the Crew Dragon or Soyuz). 2. How much does a ticket to space cost?Suborbital flights typically range from US$ 250,000 to US$ 600,000, while orbital trips to the ISS can cost tens of millions of dollars, often around US$ 55 million per person. 3. What does ‘suborbital’ versus ‘orbital’ mean?A suborbital flight briefly exits the atmosphere and returns, offering minutes of weightlessness. An orbital flight circles the Earth at high speed (about 17,500 mph) and can last from hours to weeks. 4. Is space tourism safe? What training is required?While companies emphasize safety, spaceflight remains inherently risky. Passengers typically undergo medical screening, G-force training, and simulator sessions to prepare for launch and microgravity. Risks include launch failures, radiation exposure, and harsh re-entry conditions. 5. How many people have already traveled to space as tourists?Since 2001, only a small number of individuals—both suborbital and orbital travelers—have been space tourists. Orbital tourists were rare until recent SpaceX missions, while suborbital flights are becoming more frequent, with figures still in the dozens rather than hundreds.

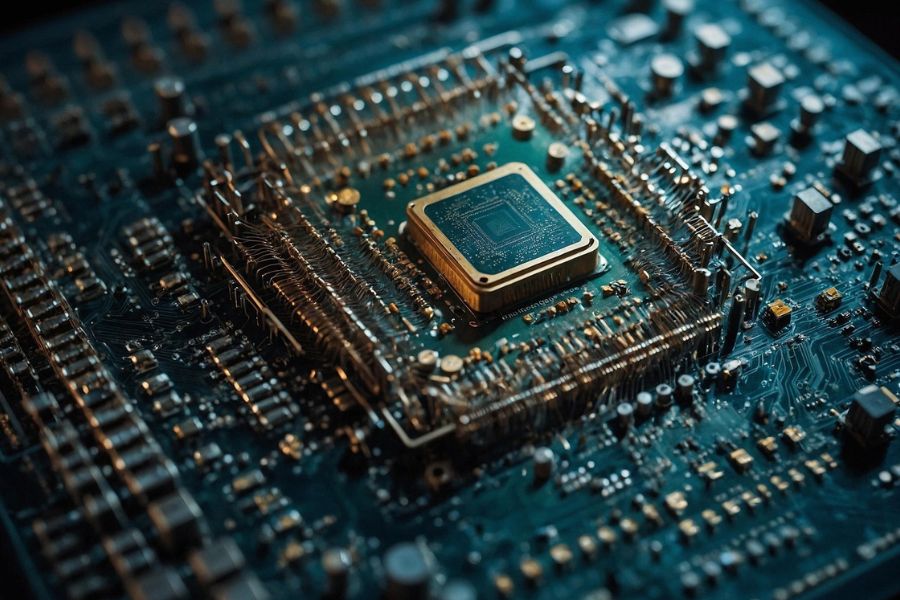

India’s semiconductor mission shifts focus to chip design and IP

Unveiling the next chapter of India’s semiconductor journey, PM Narendra Modi pledged to overhaul the design-linked incentive scheme to strengthen chip design and IP capabilities. With projects worth $18 billion already in motion, India is gearing up to capture a significant slice of the trillion-dollar global chip market. Prime Minister Narendra Modi on Tuesday announced that India is entering the next phase of its semiconductor mission with a sharper emphasis on chip design and intellectual property creation. Central to this transition is a planned revamp of the government’s design-linked incentive (DLI) scheme, a move aimed at strengthening India’s foothold in the trillion-dollar global semiconductor market. Revamping the DLI Scheme Launched in 2021 with an allocation of ₹1,000 crore, the DLI scheme was envisioned as a catalyst for startups to build chip designs and secure patents. However, uptake has been sluggish, with only 23 projects approved in three years. Industry experts have argued that the current structure—providing up to ₹15 crore per startup and a sales-linked incentive capped at ₹30 crore—was insufficient to attract deep-tech entrepreneurs who require higher-risk capital and long-term support. By promising a reset, Modi indicated that these shortcomings will be addressed. The revamped scheme will align with India’s broader ambition of shifting from being a global reservoir of semiconductor design talent to becoming a creator of intellectual property. “Today, India contributes 20% of the world’s semiconductor design talent,” he said, calling on small firms and startups to seize this historic opportunity. Drawing an analogy, Modi stated: “Oil is black gold, but chips are digital diamonds. Oil shaped the previous century, but the power of the 21st century is concentrated in the small chip.” He highlighted that the global semiconductor market, already worth $600 billion, is projected to exceed $1 trillion in the coming years, and India is poised to secure a meaningful share. Building a comprehensive semiconductor ecosystem The India Semiconductor Mission, approved in December 2021 with a ₹76,000 crore outlay, laid the foundation for this ambition. Of this, ₹65,000 crore was allocated to fabrication units and ₹10,000 crore to upgrade the Semi-Conductor Laboratory in Mohali. But Modi emphasized that the next phase is not confined to a single fab or project. Instead, the goal is to create a comprehensive ecosystem covering design, manufacturing, packaging, and high-tech device production. Currently, 10 semiconductor projects worth over $18 billion (₹1.5 lakh crore) are underway. “This reflects the growing global trust in India,” Modi said. He underscored the importance of shortening the journey from “file to factory” so that wafer production can commence faster. Union Electronics and IT Minister Ashwini Vaishnaw added that five domestic projects are already under construction and progressing swiftly. “The pilot line of one unit (CG Power) is completed, while two more units are expected to start production in the coming months. The foundation of this foundational industry has been laid very well,” he noted. Cutting red tape and building infrastructure The government has introduced several reforms to reduce bureaucratic hurdles. A national single-window system now enables companies to obtain both central and state clearances online. Additionally, semiconductor parks with plug-and-play facilities are being developed, ensuring easy access to land, power, ports, airports, and skilled labor. Modi said these measures are helping India move beyond its traditional role in backend operations toward becoming a full-stack semiconductor nation. He highlighted progress at design centers in Noida and Bengaluru, which are developing some of the world’s most advanced chips, capable of storing billions of transistors and powering immersive technologies. Meanwhile, test chips from global majors such as Micron Technology and Tata Electronics are already in production, with commercial manufacturing expected to begin later this year. While acknowledging that India entered the semiconductor race later than other nations, Modi expressed confidence in the country’s trajectory. “Our journey may have started late, but nothing can stop it now,” he said. “The world trusts India, the world believes in India, and the world is ready to build the semiconductor future with India.” With the revamp of the DLI scheme, the acceleration of fabrication projects, and the establishment of robust infrastructure, India is positioning itself not just as a participant but as a leader in the semiconductor revolution of the 21st century. FAQs 1. What is the revamped DLI scheme?A government initiative to boost chip design and IP creation by offering stronger support for startups and innovators. 2. Why is this important for India?It positions India to secure a share of the $1 trillion global semiconductor market. 3. What progress has been made so far?10 projects worth $18 billion are underway, with pilot production started at some units. 4. How is the government supporting companies?Through faster clearances, semiconductor parks, and plug-and-play infrastructure. 5. Why focus on chip design and IP?To move beyond talent contribution and ensure India owns and profits from semiconductor innovations.

Why some states outpace others in two-wheeler EV adoption

Electric two-wheelers are gaining traction in India, but adoption is not uniform across states. An RBI study shows that where governments provide subsidies and charging support, people are switching to EVs much faster. In contrast, states with weaker incentives are lagging, highlighting how local policies and affordability directly shape India’s clean mobility journey. India’s transition to electric mobility is at a crucial juncture. With transport contributing significantly to emissions and dependence on fossil fuels, the push for electric vehicles (EVs) has become both an environmental and economic priority. Within this shift, the two-wheeler segment is particularly important because of its scale and affordability. A recent Reserve Bank of India (RBI) analysis reveals that state-level financial incentives are playing a decisive role in shaping how quickly Indians adopt electric two-wheelers. The RBI study compared adoption patterns across 23 states and found a stark difference between those offering direct financial subsidies and those relying only on tax and registration waivers. In September 2023, states that provided only waivers saw two-wheeler EV adoption drop by almost a quarter on a quarter-to-quarter basis. Meanwhile, states that supplemented waivers with direct subsidies recorded a smaller decline of around 17%. This indicates that subsidies remain critical in cushioning the impact of reduced support at the national level, particularly after adjustments in the FAME II scheme. This finding is especially significant because the two-wheeler market in India is highly price-sensitive. For most households, affordability is the single biggest determinant of purchase decisions. Subsidies, by lowering the upfront cost, make EVs a more accessible choice for a larger pool of consumers. The study also highlights regional disparities. Southern and Western states- many of which were early to adopt EV-friendly policies -regularly record higher-than-average adoption rates. By contrast, Northern and Eastern states lag behind, revealing the uneven pace of transition across the country. This reflects not only differences in financial incentives but also in local policy implementation, infrastructure readiness, and consumer awareness. Charging infrastructure critical enabler of EV adoption Alongside subsidies, charging infrastructure has emerged as a critical enabler of adoption. The presence of reliable charging facilities boosts consumer confidence in making the switch to electric mobility. States such as Karnataka, Goa, and Maharashtra in the west and southwest, along with Delhi and Haryana in the north, are leading in terms of charging infrastructure availability. Their success underlines the importance of complementing financial incentives with visible infrastructure that reassures buyers of practicality and convenience. Some states have gone a step further by offering capital subsidies for setting up charging stations. Andhra Pradesh, Assam, Bihar, Chhattisgarh, Gujarat, and Kerala provide between 25 and 60% of equipment costs as subsidy. Delhi has taken an even more ambitious step, providing full financial support for charging equipment. These measures ensure that infrastructure grows in tandem with demand, preventing bottlenecks that might otherwise slow adoption. While subsidies and infrastructure are central, broader dynamics also shape the EV adoption. The Institute for Energy Economics and Financial Analysis (IEEFA) estimates that each rupee invested in EVs can generate up to 21 rupees of economic value, reflecting the sector’s ability to spur innovation, jobs, and ancillary industries. At the same time, consumer studies have found that while subsidies strongly influence purchase decisions, challenges like limited model availability, concerns about vehicle safety, and patchy charging networks remain obstacles to mass adoption. National-level efforts, especially through the FAME II scheme, have also been instrumental. Since its launch in 2019, FAME II has channeled significant funding into demand incentives and charging infrastructure. Yet adoption has not been uniform, with some states failing to build the ecosystem needed to sustain growth once subsidies are reduced. For example, in Andhra Pradesh, EV penetration over the past five years has been well below the national average, illustrating how uneven implementation can limit progress. India’s EV sales nearly doubled in 2023 Despite these challenges, the momentum is undeniable. India’s EV sales nearly doubled in 2023 and are projected to rise by two-thirds in 2024, driven largely by the two-wheeler segment. However, looming policy decisions, such as a possible increase in GST on premium EVs, could disrupt this trajectory if not carefully managed. The RBI study reinforces a crucial lesson: state-level policies are as important as national schemes in shaping EV adoption. Where states combine subsidies with strong infrastructure support, adoption rates are resilient even in the face of reduced central incentives. Conversely, in regions where state-level support is weaker, progress is slower and more vulnerable to policy changes. India’s two-wheeler EV transition is a socio-economic transformation. Success depends on aligning affordability, infrastructure, and consumer awareness. State governments are proving to be powerful catalysts, with subsidies and infrastructure support directly influencing adoption rates. Going forward, a coordinated approach between the centre and the states will be essential to ensure that EV adoption is broad-based, inclusive, and sustainable. By combining national ambition with state-level execution, India can turn its two-wheeler EV revolution into a model for other emerging markets, accelerating its journey toward cleaner mobility and a greener future. FAQs on electric two-wheeler adoption in India 1. Why are electric two-wheelers more popular in some states than others? State-level incentives—like subsidies, tax waivers, and support for charging infrastructure—play a major role in driving faster EV adoption. 2. What is the current market share and growth outlook for electric two-wheelers in India? As of FY2025, two-wheelers made up close to 60% of India’s total EV market, with penetration rising from 6–7% to potentially 30–40% by 2030. 3. How much do electric two-wheelers cost compared to petrol bikes, and what are the running cost savings? Although the purchase price is relatively higher, EVs offer major cost savings—electric models can cost as little as ₹0.50/km versus ₹2–5 per km for petrol scooters. 4. What are the main challenges hindering mass adoption of electric two-wheelers? Key barriers include the high upfront cost, limited charging infrastructure in many regions, consumer skepticism regarding battery life, and uneven policy support. 5. Which states are leading in two-wheeler EV adoption and what incentives

From Paris to Seoul, beauty giants are betting on Indian spenders

India’s beauty industry is at an inflection point, transforming rapidly with a surge in premium international imports reshaping consumer habits. The country’s beauty and personal care industry, valued at US$ 21 billion in 2023, is projected to grow to US$ 34 billion by 2028. Global beauty giants like L’Oréal, Estée Lauder, Shiseido, and Amorepacific are seizing this momentum, positioning India as their next growth frontier. Fueled by social media trends and e-commerce platforms, the market is evolving into one of the world’s fastest-growing beauty hubs. Not too long ago, most of us grew up peeking into our mothers’ vanities and finding a familiar lineup of local creams, a talc with a floral puff, a kajal pencil that seemed to last forever. Our mothers and grandmothers relied on a few familiar staples, and that was enough. Beauty was simple, predictable, and almost entirely local. Today, the shelves look very different. We’re buying the same eyeshadow palettes our favourite influencers use, a gloss bomb from Sephora to keep lips plump, and even snail mucin which was once a distant dream to achieve that glass skin. The walls between “their beauty world” and “ours” have all but disappeared, with teenagers in India just as invested in multi-step routines as their K-pop idols and pop icons. This shift is more than a change in brands—it reflects how aspirations have evolved with rising incomes, international exposure, and a young, confident consumer base. India’s beauty and personal care industry, valued at US$ 21 billion in 2023, is projected to grow to US$ 34 billion by 2028, making it one of the fastest-growing beauty markets worldwide. Global beauty giants like L’Oréal, Estée Lauder, Shiseido, and Amorepacific are capitalizing on this momentum, positioning India as their next growth frontier. For these companies, India is one of the last major untapped consumer markets, offering fresh opportunities at a time when demand in developed economies is plateauing. Global trends shaping Indian beauty That blurring of boundaries has been fueled by global currents, particularly from East Asia and the US. Korean skincare has moved from niche to mainstream, with sheet masks, essences, and serums now common in Indian routines. China and the US too have become important sources of premium imports, adding to the mix of international influences shaping the market. Social media has done the heavy lifting in this transformation. A lipstick shade can leap from a K-drama close-up to Indian shopping carts in a matter of days, while Instagram reels, YouTube reviews, and TikTok hacks turn new products into household names almost overnight. E-commerce has taken care of the rest — platforms like Nykaa, Amazon, and have broken the metro monopoly, making premium beauty just as accessible in smaller cities as it is in Delhi or Mumbai. The rising appetite for premium beauty The rising appetite for premium beauty is reflected in import trends. Imports of cosmetics and skincare rose from US$ 80.9 million in FY20 to US$ 171.9 million in FY25, according to the Ministry of Commerce and Industry. Korean skincare products alone have been expanding at an annual growth rate of 63%, with import volumes quadrupling since 2020. Breaking down imports by category: Lip makeup preparations led with US$ 61.2 million, with China, Belgium, the US, South Korea, and the UAE as key suppliers. Face creams surged nearly sevenfold to US$ 53.6 million in FY25, from US$ 7.7 million in FY20, with China and South Korea as top sources. Eye makeup imports reached US$ 34.5 million, while perfume imports rose 64.2% to US$ 171.1 million in FY25. Within this broader growth, the luxury beauty segment—currently only 4% of the market holds the greatest promise. From US$ 800 million in 2023, it is projected to grow fivefold to US$ 4 billion by 2035. Industry analysts describe India as “the last bastion of growth for premium beauty,” underscoring its strategic importance for global players. India’s beauty products exports and imports value (2020-2024) Source: tradeimex.in, Figures in US$ Billion * From imports to local manufacturing As demand accelerates, many international brands are localizing production to reduce costs, improve supply chain resilience, and cater more effectively to Indian consumers. L’Oréal India now manufactures over 95% of its sold products domestically. CeraVe, a popular skincare brand, began local production in 2025 while simultaneously starting exports to 11 countries. Other brands are exploring hybrid models—importing high-value luxury products while producing mid-range items locally. This shift not only supports the government’s Make in India initiative but also signals the country’s growing role as a manufacturing hub for global cosmetics. Customization for Indian consumers International players are learning quickly that winning in India isn’t about copy-pasting global playbooks — it’s about listening to local beauty habits and weaving them into their own strategies. Product innovation: Kohl has been part of Indian makeup for generations, so when global brands launch sleek, kohl-based eyeliners, they aren’t just adding another product — they’re acknowledging a ritual that’s deeply familiar. The same goes for herbal-infused creams or glow-enhancing formulas that work in India’s heat and humidity. These touches make an international brand feel less distant, more like something that belongs on an Indian dressing table. Cultural collaborations: The Estée Lauder x Sabyasachi partnership is a perfect example. It was about blending global luxury with Indian craftsmanship, something consumers could connect with emotionally. Their investment in Forest Essentials goes even deeper — tying a global beauty powerhouse to Ayurveda-inspired luxury that already had strong cultural roots. Moves like these show respect for Indian tradition, rather than trying to overwrite it. Data-driven expansion: Then there’s the way brands are now looking beyond Delhi and Mumbai. Digital analytics help them spot beauty conversations bubbling up in places like Siliguri or Lucknow, where a new wave of premium buyers is emerging. By understanding what people in these cities are searching, watching, or adding to wishlists, brands can tailor launches that feel relevant rather than imposed. Retail partnerships: And of course, Nykaa has become the go-to gateway. For global names like NARS, it’s

Can biofuels clean up India’s hard-to-abate industries?

Steel and cement are at the heart of India’s development, but also among its biggest climate challenges. Together, they account for a significant share of global CO₂ emissions, and India, as the world’s second-largest producer of both, faces mounting pressure to clean them up. This blog looks at the current state of these industries — their heavy reliance on coal and the regulatory norms they must now comply with. It then explores how biofuels can step in: from co-firing biomass in cement kilns and biochar trials in steel furnaces, to cutting transport emissions with bio-CNG. Finally, we examine the opportunities and challenges ahead, and why biofuels could be a crucial bridge in helping India balance growth with sustainability. Steel and cement are the backbone of India’s growth story. They build highways, homes, factories, and metros — but they also come with a heavy climate cost. Together, the two industries contribute close to 15% of global CO₂ emissions. India, the world’s second-largest producer of both, churns out around 125–130 million tonnes of steel and over 400 million tonnes of cement every year. And with mega projects under the National Infrastructure Pipeline (NIP) and “Housing for All” on the horizon, demand is only set to grow. That growth, however, collides with India’s climate commitments. The country has pledged to reach net zero by 2070 and to cut the emissions intensity of GDP by 45% by 2030. For “hard-to-abate” sectors like steel and cement, decarbonisation is not just desirable — it’s unavoidable. Coal dependence and compliance pressure At present, both industries are deeply tied to fossil fuels: Cement: Kilns consume up to 100 kg of coal per tonne of cement. Most plants in India still rely on coal and petcoke, with Thermal Substitution Rates (TSR) from alternative fuels below 10% — far behind the 40%+ achieved in Europe. Steel: Over 90% of India’s steel is made via the blast furnace–basic oxygen furnace (BF-BOF) route, which depends heavily on coking coal, most of it imported. This dependence exposes companies not only to high emissions but also to volatile global fuel prices. Regulators are already tightening the screws: The Ministry of Environment, Forest and Climate Change (MoEFCC) has enforced stricter norms on NOx, SOx, and particulate matter for cement. States like Haryana and Punjab have even mandated the use of crop residues in kilns to fight stubble burning. The Ministry of Steel has floated a National Green Steel Policy, and Indian exporters face pressure from the EU’s Carbon Border Adjustment Mechanism (CBAM), which could impose hefty carbon taxes on emissions-heavy imports. Both sectors are also covered under the Perform, Achieve and Trade (PAT) scheme, which sets efficiency targets and creates a carbon trading mechanism. In short, business-as-usual is no longer viable. The role of biofuels While long-term solutions like green hydrogen and carbon capture are still maturing, biofuels present a near-term, practical option. They don’t require a complete overhaul of existing systems and can be integrated relatively quickly. In Cement: Agricultural residues (rice husk, sugarcane trash, sawdust) and Refuse-Derived Fuel (RDF) can co-fire alongside coal in kilns. Majors like Dalmia Cement and ACC have already piloted biomass co-firing. Wider adoption could push India’s TSR closer to European levels. In Steel: Trials with biochar and bio-coke are underway at Tata Steel and JSW. These could partially replace fossil coking coal in blast furnaces, cutting emissions while reducing import dependence. In Logistics: Both industries move massive volumes of raw materials and finished goods. Using bio-CNG or biodiesel trucks can reduce Scope 3 emissions, a growing part of sustainability reporting. Why biofuels make sense for India India produces over 230 million tonnes of agricultural residues every year, much of which is burned in fields, choking cities with smog. Redirecting this biomass into cement kilns, blast furnaces, and trucks delivers a triple dividend: Extra income for farmers. Lower carbon footprint for industry. Cleaner air for cities. Government support is already in place. The SATAT scheme promotes compressed biogas (CBG), and several state policies incentivize biomass use in industries. By tapping into these policies, Indian producers can cut emissions while strengthening their global competitiveness. Fragmented biomass supply chains, inconsistent quality, and higher costs compared to cheap coal are real hurdles. But these challenges are surmountable with investment in logistics, standardisation, and policy incentives. The bigger point is this: biofuels may not replace every tonne of coal, but they buy time. They provide industries with a compliance pathway today while preparing for a future where hydrogen, CCUS, and circular practices take centre stage. For exporters, especially to Europe, early adoption can mean the difference between paying carbon taxes or enjoying preferential access to markets. India’s steel and cement sectors stand at a crossroads. The world is moving toward low-carbon materials, and buyers are willing to pay a premium for them. Biofuels are not the endgame, but they are a crucial first step — a bridge technology that allows India to align growth with climate goals, keep industries competitive, and turn what are now climate problems into climate solutions. FAQs 1. Why are steel and cement considered “hard-to-abate” industries? Steel and cement require extremely high temperatures for production, which are currently met using coal and petcoke. Over 90% of India’s steel is produced through the coal-intensive BF–BOF route, while cement kilns consume up to 100 kg of coal per tonne. This reliance makes emissions reduction difficult, earning them the label “hard-to-abate.” 2. How can biofuels reduce emissions in the cement industry? Biofuels like biomass pellets, agri-residues, and Refuse-Derived Fuel (RDF) can substitute coal in cement kilns. By increasing the Thermal Substitution Rate (TSR), cement plants can significantly lower their carbon footprint. Companies like Dalmia Cement and ACC are already experimenting with rice husk, sawdust, and RDF co-firing. 3. What role can biofuels play in steel production? Biochar and bio-coke are being tested as partial substitutes for coking coal in blast furnaces. Trials by companies like Tata Steel and JSW show that biofuels could cut emissions and reduce India’s heavy import dependence

India’s industrial production growth accelerates to 4-month high of 3.5% in July

India’s industrial production rose to a four-month high of 3.5% in July, driven by a strong showing from the manufacturing sector, according to official data released on Thursday. The last time the country recorded comparable growth was in March 2025, when industrial output increased by 3.9%. In contrast, factory output, measured by the Index of Industrial Production (IIP), had grown by a sharper 5% in July 2024. India’s industrial output gained momentum in July 2025, rising to a four-month high of 3.5%, aided largely by the robust performance of the manufacturing sector. The latest figures released by the National Statistical Office (NSO) highlight a notable recovery in factory activity after months of subdued growth, offering cautious optimism for the economy amid mixed signals from other core sectors. This marks the highest level of growth since March 2025, when industrial production had climbed by 3.9%. In comparison, the growth rate in July 2024 was much stronger at 5%, reflecting the challenges faced by industries over the past year. Manufacturing Leads the Charge The standout performer in July was the manufacturing sector, which registered a growth of 5.4%, up from 4.7% in July 2024. Manufacturing accounts for the bulk of India’s industrial output, and its healthy performance underscores resilience in consumer demand as well as improved capacity utilization by companies. Experts attribute this expansion partly to sustained domestic consumption in urban areas, gradual improvements in rural demand, and continued government support through production-linked incentive (PLI) schemes. Key industries such as automobiles, pharmaceuticals, textiles, and chemicals have reported stronger outputs, aided by both domestic sales and export demand in select categories. However, the overall picture was tempered by a sharp contraction in mining output, which fell 7.2% in July 2025 compared to a healthy growth of 3.8% in the same month last year. Analysts suggest that lower coal and mineral production due to weather-related disruptions and operational bottlenecks were the main contributors to the decline. The power sector also showed weakness, expanding by only 0.6% compared to a robust 7.9% growth in July 2024. The tepid performance reflects both lower electricity demand during the monsoon season and supply-side issues, including fluctuations in coal availability and delayed capacity additions in renewable energy projects. Looking at the broader fiscal year performance, the industrial sector grew by 2.3% during April–July FY26, significantly slower than the 5.4% growth recorded during the same period in FY25. This indicates that despite the July rebound, industrial activity has yet to regain sustained momentum. Economists caution that while the manufacturing-led recovery is encouraging, the persistent weaknesses in mining and power production pose risks to maintaining a steady growth trajectory. Since these sectors are critical inputs for industrial activity, their underperformance could limit the scope of a broad-based recovery. Broader Economic Context The industrial production data comes at a time when India is navigating a complex economic landscape. On the one hand, inflationary pressures have eased somewhat, giving room for consumer demand to stabilize. On the other hand, global economic uncertainties, weak external demand, and volatile commodity prices are weighing on the outlook for exports and raw material costs. The manufacturing sector’s resilience also aligns with broader government efforts to boost domestic production, reduce import dependency, and position India as a global manufacturing hub. Initiatives such as the Make in India program and the expansion of the PLI scheme are gradually beginning to reflect in sectoral data, though challenges remain in infrastructure, logistics, and energy reliability. Outlook Going forward, analysts believe that the trajectory of industrial growth will depend heavily on three factors: Sustained manufacturing momentum – If consumer demand, both domestic and export-oriented, continues to hold, the sector could remain the key driver of industrial growth. Revival in mining and power sectors – Improving coal output, diversifying mineral production, and strengthening renewable energy capacity will be crucial for a balanced recovery. Policy and investment climate – Continued reforms, infrastructure development, and stable macroeconomic policies will help attract investments and support long-term industrial expansion. In conclusion, the industrial production growth of 3.5% in July 2025 signals a welcome rebound, largely powered by manufacturing. However, the contraction in mining and sluggish power generation highlight vulnerabilities that policymakers must address. With the right support, India has the potential to not only sustain but also accelerate industrial growth, thereby reinforcing its role as one of the world’s fastest-growing major economies.

From Kyoto to Kolkata: The untold story of Matcha’s rise in India

India may be a chai nation, but matcha is steadily making space on its menus. Once reserved for Japanese tea ceremonies, the green tea has become a global lifestyle product and young Indians are driving its entry here through cafés, online brands, and social media. In Japan, matcha is part of a ceremony. The bright green powder is whisked with a bamboo brush until it turns into a smooth, frothy drink. This ritual made matcha a symbol of respect and mindfulness in Japanese culture. Over the past two decades, matcha has moved from tea rooms in Kyoto to café counters in New York and wellness aisles in London. The global matcha market was valued at US$ 3.4 billion in 2023 and is expected to cross US$ 6 billion by 2030. No longer confined to tradition, it is now sold in lattes, smoothies, cookies, protein bars, and even skincare products turning an ancient ritual into a worldwide lifestyle trend. Unlike coffee, which gives a quick jolt of energy and often a crash, matcha delivers a slower, steadier release of caffeine which is due to the amino acid L-theanine. That’s why many young consumers see it as a “smarter coffee” and giving the bursts of energy without the jitters. Interestingly, matcha is now making waves in India which has forever been ruled by tea. For India, a nation of cutting chai at tapris, spiced masala brews at home, and steaming cups passed around office canteens, matcha is both familiar and foreign The Matcha craze: Health, aesthetics, aspiration In the 2000s, coffee chains changed how urban India drank coffee and matcha is beginning to do something similar for today’s youth. Millennials and Gen Z are driving the demand in pursuit of building a lifestyle. Part of the appeal lies in matcha’s image: clean, energising, and Insta-friendly. Its distinct green hue makes it camera-ready, and its antioxidant-rich reputation makes it a popular choice. In a world where wellness is taking over matcha is a badge. This blend of health consciousness, global exposure, and social media trends is what’s propelling the matcha wave. It’s no surprise then that the matcha tea market in India, valued at US$ 104 million in 2024, is projected to grow at a CAGR of 8.6% to reach US$ 167.8 million by 2030. Unlike chai, which is deeply local, matcha’s rise in India is powered by both cafés and clicks. Chains like Starbucks and Third Wave Coffee introduced matcha lattes as aspirational beverages the kind you try when you want to look adventurous or get a taste of International beverages. At the same time, online-first brands have been educating consumers on how to buy, whisk, and cook with it. In 2024, 41% of India’s matcha sales came from online channels, as D2C brands tapped into Instagram reels, YouTube tutorials, and influencer tie-ups to tell the “green gold” story. The offline retail story is catching up too. Modern grocery stores and organic food shops in metros now stock multiple matcha brands, often placed next to green teas and herbal infusions turning curiosity into impulse buys. In 2024, the powdered form of matcha held a 53.75% revenue share of the Indian matcha tea market in 2024, making it the largest product segment. Beyond whisked tea, it’s slipped into ice creams, cookies, protein bars, health supplements, and fusion desserts. The instant premix category is growing fastest for first time buyers designed for young urban professionals who want the benefits followed by the ceremonial high grade matcha for the regular drinkers. And in India, where taste matters as much as health, brands are experimenting with local twists — from matcha kulfi to cardamom matcha blends. Still, challenges remain. High-quality ceremonial matcha is expensive, often imported from Japan. That makes it several times costlier than regular tea, restricting it to urban elites. Taste is another hurdle. For a country raised on sweet and spiced chai, matcha’s earthy, slightly bitter flavour is unfamiliar. Brands are trying to bridge the gap with sweetened lattes, flavoured blends, and dessert-style infusions. Interestingly, there’s an untapped opportunity in domestic cultivation. With tea-growing belts in Assam, Darjeeling, and Nilgiris, India has the potential to produce its own matcha. Local production could cut costs, create a “Made in India” identity, and even open doors to exports. Will matcha replace chai? Will matcha replace chai? Probably not. But it doesn’t need to. What’s happening instead is coexistence. Chai remains comfort, routine, and nostalgia. Matcha represents aspiration, wellness, and global belonging. Over the next few years, expect three big shifts: Mass reach: affordable matcha premixes targeting tier-2 and tier-3 cities. Diversification: more matcha in nutraceuticals, beauty, and even fitness products. Localisation: Indian-grown matcha building both domestic and global credibility. As India’s youth balance heritage with modern lifestyles, matcha captures that tension perfectly, it’s global, aspirational, and just experimental enough to feel fresh. But for matcha to truly move beyond cafés and Instagram and become part of everyday life, it will need innovation. Brands will have to create formats that are easy to adopt and simple to fold into daily routines. FAQs on Matcha Tea in India 1. Why is matcha becoming popular in India? Matcha is gaining popularity in India because it combines health benefits with lifestyle appeal. Its antioxidant-rich profile, steady energy release (without coffee jitters), and Instagram-friendly aesthetic make it especially attractive to millennials and Gen Z. 2. How is matcha different from green tea and coffee? Unlike regular green tea, matcha uses whole tea leaves ground into a fine powder, making it richer in nutrients and antioxidants. Compared to coffee, matcha provides a calmer, longer-lasting energy boost thanks to the amino acid L-theanine, which balances caffeine. 3. What is the size of the matcha tea market in India? India’s matcha tea market was valued at US$ 104 million in 2024 and is expected to reach US$ 167.8 million by 2030, growing at a CAGR of 8.6%. This growth is driven by rising health awareness, café culture, and online-first brands. 4. Is matcha

From LEDs to AI: the rise of vertical farming equipment

The global vertical farming equipment market hit US$ 4.2 billion in 2024 and is projected to reach US$ 29.7 billion by 2033, growing at a CAGR of 21.4%. Driven by rapid urbanization, technological advancements, and rising investments from agri-tech startups and government initiatives, innovations like energy-efficient LED lighting, AI-driven crop analytics, and IoT monitoring are boosting productivity while conserving water and reducing pesticide use. Image Source: Freepik The global vertical farming equipment market reached a value of US$ 4.2 billion in 2024, highlighting strong momentum in the sector, driven largely by rapid urbanization and technological innovations in controlled environment agriculture. The market is projected to grow at an impressive CAGR of 21.4% between 2025 and 2033, with estimates suggesting it will reach US$ 29.7 billion by 2033. Vertical farming equipment encompasses a range of specialized tools, machinery, and systems that make large-scale vertical agriculture possible. This includes hydroponics, aeroponics, aquaponics, irrigation devices, climate control systems, sensors, and artificial lighting solutions. Increased investments from agri-tech startups, together with government initiatives supporting smart agriculture, are significantly fueling the demand for advanced equipment. One of the most impactful developments has been the emergence of energy-efficient LED lighting systems designed specifically for plant growth, which has substantially lowered operational expenses. Alongside this, the adoption of AI-powered crop analytics, robotics, and IoT-enabled monitoring systems has enhanced productivity, crop yield, and consistency. Furthermore, vertical farming cuts water consumption by as much as 90% compared to conventional farming methods and removes the reliance on harmful pesticides. As sustainability concerns rise, eco-friendly farming equipment is gaining greater traction globally. Vertical farming itself has revolutionized crop cultivation by utilizing vertically stacked layers or structures that maximize space within a limited footprint. It incorporates cutting-edge techniques such as hydroponics, which enables soil-free cultivation; aeroponics, where plants are suspended and their roots misted with nutrients; and artificial lighting to replicate optimal growth conditions. By carefully controlling environmental factors like light, temperature, and humidity, vertical farming enables crops to thrive more effectively than in traditional soil-based agriculture. This model is especially advantageous in urban regions where arable land is limited, making it a key solution for future food security. Market segmentation By Equipment Type: Lighting Systems – High-performance LEDs and grow lights tailored for photosynthesis. Climate Control Systems – HVAC units, sensors, and automated controllers for regulating temperature and humidity. Hydroponic and Aeroponic Systems – Soil-less growing platforms ensuring efficient nutrient delivery. Irrigation Systems – Automated drip and mist irrigation technologies designed to optimize water usage. By Crop Type: Vertical farming equipment is widely used for leafy greens, herbs, tomatoes, strawberries, and microgreens. With ongoing advancements, production of cereals and staple crops are also becoming increasingly feasible. By Geography: North America – Leading adoption driven by agri-tech startups and strong urbanization trends. Europe – Growth supported by sustainability policies and renewable energy integration. Asia-Pacific – Fastest-growing market, spurred by dense populations, limited arable land, and food security imperatives. Challenges faced by market Despite its strong growth prospects, the vertical farming equipment market continues to face several challenges that could hinder widespread adoption and scalability. High initial investment costs – Setting up vertical farming systems involves significant upfront expenditure on advanced equipment such as LED grow lights, climate control systems, hydroponic or aeroponic setups, and automated irrigation systems. For commercial-scale projects, the cost of infrastructure, technology integration, and energy optimization can be prohibitively high. While long-term returns are promising due to higher yields and efficient resource utilization, the heavy capital requirements often deter small and medium-scale farmers and make it difficult for the industry to achieve faster penetration. Energy consumption – Although vertical farms rely on energy-efficient LED lighting, the overall power demand in large-scale facilities remains considerable. Continuous artificial lighting, HVAC systems for climate control, and automated irrigation or nutrient delivery systems drive up electricity costs. In regions where renewable energy is not widely accessible or subsidized, these expenses can significantly impact profitability. Energy remains one of the most critical operational challenges that must be addressed for vertical farming to become more economically viable. Technical expertise – Operating and maintaining vertical farming systems requires specialized knowledge of advanced technologies such as hydroponics, aeroponics, AI-driven monitoring, and IoT-based automation. Skilled professionals are needed to manage equipment calibration, crop health monitoring, and system troubleshooting. However, the availability of such expertise is limited in many developing economies, creating a barrier to adoption. Without adequate training programs and knowledge transfer, scaling vertical farming at a global level may face setbacks. Collectively, these challenges highlight the importance of innovation, policy support, and cost optimization. Addressing these hurdles through research and development, government incentives, affordable renewable energy integration, and capacity building for skilled labor will be crucial to ensuring that vertical farming fulfills its potential as a sustainable and scalable food production system. Future outlook The vertical farming equipment market is expected to expand rapidly as smart farming technologies evolve. The integration of renewable energy solutions, AI-driven crop monitoring, and fully automated farming systems will make vertical farming more scalable and commercially viable. Partnerships between equipment manufacturers, startups, and governments are likely to accelerate innovation, reduce costs, and broaden access, positioning vertical farming as a cornerstone of sustainable agriculture worldwide.

Flex-fuel vehicles in India: Market growth, challenges & roadmap

India’s automobile sector is gearing up for a transformative shift, with flex-fuel vehicles (FFVs) positioned as a practical bridge between petrol engines and cleaner alternatives. Backed by the government’s ambitious E20 blending target by 2025, the market is projected to touch US$ 855.77 billion, growing at a robust pace. Drawing lessons from Brazil and the US, India’s success will depend on scaling ethanol production, ensuring vehicle compatibility, upgrading fuel infrastructure, and winning consumer trust. If these elements align, FFVs could not only cut emissions and reduce fuel costs but also redefine the future of sustainable mobility in India. The automobile industry is entering a decisive phase where sustainability is shaping future mobility. Among the key innovations, flex-fuel vehicles (FFVs) have emerged as a practical bridge between conventional petrol engines and greener alternatives. Unlike traditional vehicles, FFVs can run on varying blends of petrol and ethanol—ranging from E10 (10% ethanol, 90% petrol) to E85 (85% ethanol, 15% petrol). This flexibility makes them a strong contender in India’s transition to low-emission transport. Globally, flex-fuel technology has already proven successful. Brazil leads the way, with 94% of new cars being FFVs, supported by strong agri-tech and ethanol supply chains. The United States, too, has made significant progress through policy incentives and low-cost enzyme technologies. Drawing lessons from these models, India is accelerating its ethanol blending program, targeting 20% ethanol blending (E20) by 2025, with FFVs expected to play a crucial role in meeting this goal. India’s flex-fuel vehicle (FFV) market is projected to be worth US$ 855.77 billion in 2025, expanding at a healthy CAGR of 15% between 2025 and 2030. Demand is set to rise sharply in key urban hubs such as Delhi, Mumbai, Bangalore, and Hyderabad, driven by a mix of policy incentives, technology advancements, and the urgency to curb emissions. Passenger vehicles hold the lion’s share of this market, commanding about 65% of its value, followed by commercial vehicles at 25%, with the remaining 10% spread across other segments. In terms of fuel mix, the market is composed of 70% ethanol, 20% methanol, and 10% gasoline. Automotive leaders like Tata Motors, Mahindra & Mahindra, Maruti Suzuki, and Hyundai are already making bold moves, investing in research and development to introduce models tailored for India’s ethanol-blending roadmap. With the government advancing its goal of 20% ethanol blending (E20) by the end of 2025, the next five years will determine how quickly India can align its vehicle ecosystem with this target. Growth drivers One of the strongest growth drivers for the market is environmental awareness. Ethanol produces significantly fewer carbon dioxide, nitrogen oxides, and sulphur oxides compared to petrol. According to NITI Aayog, sugarcane-based ethanol can reduce greenhouse gas emissions by up to 65%. This aligns with India’s broader climate commitments and its ambition to cut oil imports. Cost advantage is another factor tilting the balance. Ethanol is generally 20–50% cheaper than petrol, offering immediate financial relief for price-sensitive consumers. The development of advanced engine technologies is also accelerating adoption. New systems with corrosion-resistant materials, high-precision sensors, and optimized injection mechanisms are making ethanol compatibility more viable and reducing concerns about long-term wear and tear. Experts point out that India can draw lessons from global leaders in this space. As Dr. Saleem remarked, “India can work following Brazil’s model, where 94% of new cars are FFVs. India can invest in FFV vehicles as we move towards higher ethanol blends.” Brazil’s success rests on strong agri-tech support, robust fuel distribution infrastructure, and policies mandating vehicle compatibility. The United States has also advanced with low-cost enzyme technology and supportive biofuel policy, demonstrating how innovation and regulation together can scale flex-fuel adoption. India’s journey, however, is not without challenges. A key concern is vehicle compatibility. As Dr. Sanjukta Subudhi highlighted, “Vehicle compatibility is a major hurdle. Most existing vehicles are designed for E10 and are not fully compatible with E20. To bridge this gap, manufacturers like Maruti Suzuki, Tata Motors, and Hyundai are developing flex-fuel vehicles (FFVs) that can run on higher ethanol blends, with Maruti planning E20-compatible launches in 2025. Wider E20 adoption will also require an extensive rollout of compatible fuel across retail outlets and infrastructure upgrades in storage and dispensing systems. Ethanol’s chemical properties demand careful handling and robust quality control to ensure performance and safety.” This indicates that India’s transition to E20 and beyond will require coordinated action, not just from automakers, but across fuel retailing, storage, and quality control domains. Without parallel infrastructure upgrades, vehicles built for higher ethanol blends may face performance issues, undermining consumer trust. The question of readiness extends beyond vehicles and fuel stations. DS Mahal stressed the importance of systemic upgrades, noting that “India’s fleet compatibility is still below 5%, and depot readiness for E20/E30 needs major upgrades. India must now align vehicle policies (mandating E20 compatibility for all new petrol cars from April 2026), upgrade over 2,000 fuel depots and 30,000 tankers to E20 standards, and introduce pricing incentives (₹1.5–2.0/litre) to encourage consumer adoption.” Such measures are vital to ensure that flex-fuel vehicles are not just manufactured, but also supported by the supply chain and embraced by the market. Another challenge lies in consumer perception and awareness. Many Indian car owners remain skeptical about ethanol’s effect on fuel efficiency and engine longevity. Studies indicate that E20 fuel may reduce efficiency by 2–5%, though technological improvements are expected to mitigate this over time. Automakers, policymakers, and fuel distributors must work together to communicate the benefits, clarify misconceptions, and assure consumers of long-term safety. While obstacles exist, the momentum is undeniable. India’s ethanol production capacity is expanding rapidly, supported by surplus crops such as sugarcane and rice. Recently, the government redirected record rice stocks into ethanol production, underscoring how the biofuel push also provides an outlet for agricultural surplus while generating rural income. States like Gujarat are pioneering ethanol and compressed biogas (CBG) ventures, reinforcing the link between renewable fuels, rural entrepreneurship, and national energy security. The future of India’s flex-fuel vehicle market will depend on

Express logistics in India set to hit US$ 22 billion by FY30

India’s express logistics and courier sector is poised to double from US$ 9 billion in FY25 to US$ 18–22 billion by FY30, supporting up to 7.5 million jobs, according to an EICI–KPMG report. The industry, which played a vital role during the COVID-19 vaccination drive, is now central to e-commerce growth, MSME exports, and cross-border trade. The express logistics and courier sector is projected to reach US$ 18-22 billion by FY2029-30, up from an estimated US$ 9 billion in FY2024-25, and is expected to support 6.5-7.5 million jobs, according to a report. The report also highlighted that the express industry has evolved from being merely a logistics facilitator to becoming an essential service provider, playing a crucial role during the COVID-19 pandemic by supporting the world’s largest vaccination drive and ensuring priority delivery of essential goods. The report, titled “Express Industry in India 2025: Powering India’s Economy, Connecting Businesses and Markets,” commissioned by the Express Industry Council of India (EICI) and KPMG, identified five priority areas—agility and adaptability, efficiency improvements, customer centricity, a sustainable operating outlook, and a robust policy and regulatory framework—for unlocking future growth. It also emphasizes the need for targeted policy measures, infrastructure expansion, and technology adoption, supported by initiatives such as PM Gati Shakti, the National Logistics Policy, and Bharatmala Pariyojna. Post-pandemic growth is being fueled by high internet and smartphone penetration, exponential e-commerce expansion, increased MSME output, and significant infrastructure development in tier II and III cities, the report stated. It was released by Union Minister for Road Transport and Highways Nitin Gadkari, alongside senior government officials, industry leaders, and other stakeholders, at an event held in New Delhi late Tuesday. The sector has expanded from US$ 3 billion in FY17 to US$ 9 billion in FY25, achieving a CAGR of 12 to 15%. It is anticipated that the market will double to between US$ 18 and 22 billion by FY30. By FY25, the express industry is projected to support between 2.8 and 3 million jobs, the report noted. Furthermore, the sector is expected to make a substantial contribution to GST revenues, estimated at US$ 1 to 1.5 billion, and customs revenues of US$ 650 million, while serving as a vital enabler for e-commerce, MSMEs, and cross-border trade. The domestic express segment constitutes roughly 70% of the total market, valued at US$ 6.3 to 6.5 billion, with surface express accounting for the largest share. In addition to the growth projections, experts believe that the express logistics sector is becoming a backbone for India’s digital and consumption-driven economy. With B2B online marketplace is expected to reach US$ 200 billion by 2030, the demand for time-sensitive and reliable logistics solutions will continue to rise. MSMEs, which contribute nearly 30% to India’s GDP and 45% to its exports, increasingly rely on express delivery networks to access both domestic and global markets. By reducing delivery timelines, ensuring supply chain predictability, and connecting remote geographies, the express industry is not just complementing trade but also accelerating formalisation in the economy. The growth is also aligned with government priorities to reduce logistics costs as a percentage of GDP. India’s logistics costs currently stand at 13-14%, compared to 7-8% in advanced economies. Government initiatives aim to cut costs to around 8% by 2030. Express logistics players, through multimodal integration across surface, air, and coastal routes, are expected to play a decisive role in achieving this target. Another defining trend is technology adoption. From AI-driven route optimization and IoT-enabled tracking to warehouse automation and digital payments, express companies are leveraging technology to improve customer experience and operational efficiency. India Post’s introduction of OTP-based deliveries and UPI-enabled payment systems reflects how even traditional players are adapting to modern logistics needs, ensuring better accountability and reducing dependency on cash transactions. Sustainability is emerging as a parallel priority for the sector. Companies are increasingly adopting electric vehicles, biofuels, and greener packaging solutions to align with global ESG standards and India’s climate commitments. As consumers become more conscious of carbon footprints, integrating green logistics practices will become both a regulatory necessity and a competitive advantage. Finally, global opportunities are opening up for Indian logistics players. The surge in demand for “Made-in-India” products, coupled with expanding free trade agreements, is boosting the need for international express services. This is evident in the rising share of cross-border e-commerce, which is expected to touch US$ 127.31 billion in 2025 to US$ 235.01 billion by 2030, with India as a key contributor. Together, these developments underscore that the express logistics industry is not just expanding in size but also transforming in character—emerging as a strategic enabler for India’s growth story. “The express industry has become a critical pillar of India’s economy, connecting businesses and markets with speed and reliability. From supporting the world’s largest vaccination drive to enabling e-commerce, MSMEs and exports, our sector has shown agility, resilience and innovation. Domestic express, which makes up around 70 per cent of the market, is led by surface transport growth, while international express is expanding rapidly with global demand for Made-in-India products,” said Vijay Kumar, CEO, EICI. India’s express logistics industry is rapidly transforming to meet the increasing demand for fast and reliable delivery solutions, not only through air but also across road, rail, and coastal networks, said Girish Nair, Partner, Mobility and Logistics, National head – Aviation Sector, Global Lead – Airports, KPMG in India.