India’s auto sector faces a threat from rare earth magnet shortages, as inventories are expected to run out by mid-July 2025 amid China’s export restrictions, reveals a recent report by ICRA. With 85% of imports sourced from China, the crisis exposes strategic vulnerabilities. According to rating agency ICRA, the Indian and global automotive industries may encounter major disruptions, with inventories of rare earth magnets expected to be depleted by mid-July 2025 for specific applications. The shortage stems from China’s export restrictions and subsequent shipment delays, posing a serious threat to production continuity and market stability. The automotive sector, which had just recovered from the semiconductor shortage of 2021–22 that reduced passenger vehicle production by nearly 100,000 units (approximately 4%), is now facing another supply chain disruption. Neodymium-iron-boron (NdFeB) magnets, known for their high strength and efficiency, are crucial to several high-performance automotive applications. They are widely used in traction motors for electric two-wheelers and passenger vehicles, as well as in power steering motors found in both electric and internal combustion engine vehicles. In contrast, ferrite magnets—used in less demanding applications such as wiper motors, window regulators, and starter motors—are not affected by the same level of supply risk. In an effort to mitigate the impact of rare earth magnet shortages, Indian auto component manufacturers and OEMs are actively considering a range of alternatives. These include importing fully assembled electric motors from China, outsourcing rotor magnet assembly to China and re-importing the finished components, exploring alternative materials with comparable magnetic performance that are not classified as rare earths, and shifting toward magnet-free motor technologies that rely on electromagnets or other inductive systems. However, each of these solutions involves substantial logistical, regulatory, and engineering complexities. To prevent disruptions—particularly with magnet inventories expected to be exhausted by mid-July 2025—industry players will need to significantly accelerate their development, testing, and validation processes. ICRA emphasized that unless these challenges are swiftly addressed, the ongoing supply disruption could significantly impact production planning and the momentum of India’s EV transition. ICRA Senior Vice President and Group Head – Corporate Ratings, Jitin Makkar noted that the Electric two-wheeler motors in India typically cost between Rs 8,000 and Rs 15,000, depending on their power and vehicle specifications. Notably, rare earth magnets contribute to nearly 30% of the total motor cost. In FY2025, India imported about US$ 200 million worth of these magnets for both automotive and non-automotive uses, with around 85% sourced from China. Though the trade value may seem relatively small, the strategic reliance it represents is significant. This supply uncertainty has created serious challenges for production planning. He warned that continued dependence on China for these critical materials could severely impact the automobile industry, especially the rapidly growing electric vehicle segment, if not promptly addressed. Industry experts believe that India’s rare earth element (REE) crisis is more than just a supply chain hiccup—it’s a strategic alarm. China’s restrictive export licensing has created a major bottleneck, revealing the vulnerability of India’s electric vehicle (EV) ambitions as inventories shrink and approvals remain delayed. This situation highlights the risks of relying heavily on a single geopolitical source for vital materials. To build long-term resilience, India must develop a comprehensive domestic REE ecosystem. Establishing strategic reserves, fostering public-private R&D collaborations, and strengthening global partnerships should all form part of an integrated national strategy.

Centre plans to fix default AC temperature to ease power load

As India faces record-breaking electricity demand driven by extreme heat and soaring use of air conditioners, the government is preparing to introduce new guidelines to standardise default AC temperature settings. Led by the Bureau of Energy Efficiency (BEE), the move aims to improve energy efficiency, reduce stress on the power grid, and align consumer behaviour with long-term sustainability goals. Image credit: Freepik In a move aimed at enhancing energy efficiency and easing pressure on the power grid, the Indian government is preparing to introduce new regulations that would set a standard default temperature range for air conditioners. The Bureau of Energy Efficiency (BEE), under the Ministry of Power, is leading the initiative, which proposes a fixed temperature range of 20°C to 28°C for all air conditioners used in residential, commercial, and vehicular settings. The decision comes at a time when India is grappling with record-breaking electricity demand, driven largely by rising temperatures and the growing use of cooling appliances. On June 9, the country hit an all-time high in power demand at 241 GW, underscoring the urgency for interventions that can help reduce load on the grid. Officials from the Ministry of Power have indicated that consultations are ongoing with state governments and manufacturers to develop a uniform framework. Union Power Minister Manohar Lal mentioned that several states have requested the inclusion of humidity-related factors in the new guidelines, which are still under review. The government is also reportedly engaging with automakers to explore similar temperature regulations for vehicle air conditioning systems. Power Secretary Pankaj Agarwal highlighted the potential benefits of the initiative, noting that even a one-degree increase in temperature setting could result in a six percent reduction in energy consumption. Given the scale of AC usage in India—with millions of units currently in operation and many more being added annually—the cumulative impact of such a measure could be significant in easing the strain on the power infrastructure. The proposed regulation has been welcomed by industry players. A spokesperson from LG Electronics India described the move as progressive and aligned with global trends in sustainable energy. According to the spokesperson, standardising temperature settings could enhance appliance performance and durability, improve energy efficiency, and contribute to user health by encouraging more balanced indoor temperatures. While no official notification or implementation timeline has been confirmed yet, sources from BEE indicated that the plan is in an advanced stage, and stakeholder inputs are actively being incorporated before finalising the guidelines. Industry Concerns: Energy Demand Beyond Households While households and offices are the primary focus of this regulation, the broader industrial energy landscape also warrants attention. With India’s ambitions to become a US$ 5 trillion economy and a global manufacturing hub, the demand for uninterrupted and stable power supply in industrial zones has never been greater. Industries ranging from steel and cement to pharmaceuticals and electronics are power-intensive and operate on tight efficiency margins. Many stakeholders have voiced concerns about whether India’s current power infrastructure can simultaneously support the country’s rising residential cooling demand and its industrial energy requirements—especially during peak summer months. Energy analysts note that while curbing residential energy use through efficient cooling is a positive step, industrial energy consumption patterns must also be evaluated for optimization. Measures such as smart grid deployment, time-of-day tariffs, captive solar solutions, and improved demand forecasting are being increasingly recommended to ensure that the needs of both households and industries can be met without disruptions. Some experts argue that India’s current electricity infrastructure, though rapidly evolving, needs to scale faster to match the pace of electrification, urbanisation, and climate volatility. Peak load management, improved storage capabilities, and grid modernization are seen as essential components in preparing for the next wave of power demand especially as electrification expands beyond cooling into areas like EV charging and digital infrastructure. The upcoming guidelines mark a crucial step in aligning consumer behaviour with national energy goals. However, the challenge will be to ensure that such policies are complemented by broader infrastructure upgrades. Without strategic energy planning that includes residential, commercial, and industrial sectors, even well-intentioned reforms could fall short of their full potential. By mandating optimal AC temperature settings, the government not only aims to reduce pressure on the power grid but also sets a precedent for integrated energy governance. The success of this initiative may well depend on how it is communicated, implemented, and supported across sectors and whether India can keep pace with its own rising power ambitions.

Resilient workforce outlook for India amid global pressures

India’s employment outlook remains strong with a Net Employment Outlook (NEO) of 42% for Q3 2025, according to a report by Manpower Group. Key sectors driving optimism include IT, Energy & Utilities, and Financial Services, amid rising automation and AI skill demand. Regionally, North India leads hiring intent, and large organizations show strong outlooks. According to the survey, about.54% of employers plan to expand their workforce, 32% aim to maintain current staffing levels, 12% foresee a reduction, and 2% remain unsure about their hiring intentions. According to a recent employment outlook survey conducted by Manpower Group, the hiring activity across India’s corporate sector is expected to remain steady over the next three months. The survey reveals a positive sentiment among employers, particularly in the Information Technology (IT), Energy & Utilities, and Financial Services sectors, which are driving this optimism due to digital transformation and demand for skilled professionals, especially in artificial intelligence (AI). According to Sandeep Gulati, Managing Director of Manpower Group India and Middle East, the robust hiring sentiment in these sectors is a reflection of companies actively expanding and accelerating their digital journeys. He stated that as the third quarter of 2025 begins, India maintains a strong employment outlook with a Net Employment Outlook (NEO) of 42%— ranking among the highest globally. Amid global geopolitical challenges and trade disruptions, Indian employers are taking decisive action, with 82% ramping up automation investments and 67% reshaping workforce strategies to keep pace with changing skill requirements, Mr Gulati noted. The survey published by Reuters highlights that the private services sector is experiencing growth and anticipates economic gains from shifting global trade dynamics. The Net Employment Outlook (NEO) for India in the third quarter of the calendar year (Q2 of the financial year) stands at 42%, making it the second-highest globally, just behind the United Arab Emirates (UAE). The NEO is calculated by subtracting the percentage of employers expecting a decrease in staffing levels from those expecting an increase. Although the current quarter’s NEO is down by one point from the previous quarter, it has improved by 12 points year-on-year, indicating a strong recovery and growing employer confidence. Sector wise, the IT sector is expected to see significant hiring in the coming quarter, with 46% of surveyed employers planning to hire. Despite a slight year-on-year decline of 11 points, the sector continues to remain a key employment driver due to ongoing digital transformation and the growing need for AI-related skills. However, it is the Energy & Utilities sector, which is set to lead in employment growth with an NEO of 50% — marking an 18-point increase both quarter-on-quarter and year-on-year. The demand is fuelled by the sector’s transformation and its resilience amid global trade uncertainties. The Industrials & Materials sector also shows a strong outlook at 54%, followed by Financials & Real Estate at 43%, and Healthcare & Life Sciences at 38%. Regionally, the North of India leads in hiring intent with an NEO of 46%, up by 2 points from the previous quarter and 10 points from Q3 2024. The East (44%), West (41%), and South (36%), all showing strong employment prospects, follow the North. In terms of company size, large organizations with 1,000 to 4,999 employees exhibit the most optimistic hiring plans, with an NEO of 52%. While this is a 6-point decrease from the last quarter, it reflects a 10-point increase over the same period last year, indicating solid year-over-year growth. The survey also sheds light on the impact of global trade uncertainty on hiring plans, with 90% of companies factoring it into their decision-making. This influence is most evident in the Energy & Utilities (94%), Information Technology & Communication Services (93%), and Financials & Real Estate (91%) sectors. Globally, the United Arab Emirates ranks highest in employment outlook, with 48% of employers intending to hire. India follows closely at 42%, while Costa Rica ranks third with 41%. Brazil (33%) and the Netherlands (30%) complete the top five, making the Netherlands the only European nation among the global leaders in hiring outlook. The report is based on responses from 3,146 employers across India, collected in April 2025. It reveals that 54% of employers anticipate increasing their workforce, 32% intend to keep staffing levels unchanged, 12% expect a reduction, and 2% are uncertain about their hiring plans. The report concludes that the overall sentiment remains upbeat, pointing to a positive employment scenario in the months ahead.

India’s untapped 10,830 GW solar goldmine

India’s clean energy ambitions are getting a dramatic upgrade not from deserts alone, but from rooftops, ponds, plantations, highways, and even urban facades. A groundbreaking reassessment by The Energy and Resources Institute (TERI) reveals that India’s true solar potential is a staggering 10,830 GW nearly 15 times higher than previously estimated. This shift marks a turning point, as the nation pivots from large-scale solar parks to a more distributed, inclusive, and locally integrated energy vision. Image credit: Freepik India’s solar energy potential is far greater than previously understood. A new report from The Energy and Resources Institute (TERI) reveals the country holds a massive solar reservoir of 10,830 GW. This figure is nearly 15 times higher than the earlier 2014 estimate of 748 GW by the Ministry of New and Renewable Energy. TERI’s reassessment paints a much broader picture, now including diverse sources like rooftops, ponds, plantations, railway tracks, and urban structures beyond just barren lands. The leap doesn’t stem from improved sunlight, but from broader thinking. Where the earlier estimate accounted for only 3% of India’s wasteland, TERI’s latest “Reassessment of Solar Potential in India: A Macro-Level Study” looks beyond the usual — including floating solar systems on water bodies, building-integrated photovoltaics (BIPV), agri-voltaic farming models, and solar installations along highways and railway infrastructure. Here’s how TERI breaks down the 10,830 GW potential across diverse categories: This comprehensive reassessment arrives at a pivotal moment, aligning perfectly with India’s ambitious climate commitments. The nation’s updated Nationally Determined Contributions (NDCs) call for a 45% reduction in emissions intensity by 2030 (over 2005 levels) and a target of 50% cumulative installed capacity from non-fossil energy resources by the same year. Moreover, India’s net-zero target by 2070 underscores the critical need to identify and scale clean energy sources like solar to meet burgeoning demand. TERI projects India’s electricity demand to exceed 5,000 TWh by 2050, potentially reaching levels comparable to the European Union’s per capita consumption (around 9,362 TWh). In such a future, solar energy is unequivocally poised to form the backbone of India’s non-fossil energy mix. While the theoretical potential of 10,830 GW is staggering, the report pragmatically acknowledges that realisable capacity will necessitate detailed micro-level assessments. This will involve utilizing advanced GIS tools, remote sensing, and site-specific filters such as substation proximity, solar insolation, infrastructure access, and climate risk exposure. Essentially, TERI’s study provides a crucial macro-level roadmap, guiding future solar energy planning and investment across India. Comparisons and Socioeconomic Promise This re-evaluated potential places India in an exceptionally strong position globally. While countries like China currently lead in installed solar capacity, and the United States boasts vast land area, India’s sheer potential across diverse, unconventional categories provides a unique strategic advantage. It moves beyond merely installing panels in a few large solar parks to truly integrating solar into the national fabric. This distributed model could offer greater grid stability and resilience. The socioeconomic ramifications of harnessing such immense solar potential are profound. Experts predict that India’s renewable energy push, with solar at its core, could generate millions of green jobs across the value chain—from manufacturing components and installation to maintenance and research. This provides opportunities for skilling a young workforce, particularly in rural areas, fostering localized economies. Furthermore, widespread solar adoption reduces India’s reliance on volatile fossil fuel imports, significantly enhancing energy security and saving valuable foreign exchange. It also paves the way for greater energy access in remote and underserved communities, bridging existing power disparities. Solar projects and pilots The innovative Canal-Top Solar Power Project on the Narmada Canal in Gujarat is a pioneering project, launched in 2012, was one of the world’s first to install solar panels directly over irrigation canals. It not only generates clean electricity but also significantly reduces water evaporation from the canal below, addressing two critical challenges simultaneously. Similarly, the floating solar park at Ramagundam, Telangana, operated by NTPC, exemplifies the realization of potential beyond land. Covering reservoirs, it harnesses space that would otherwise be unused, reduces water evaporation, and maintains panel efficiency due to cooling from the water. These instances, alongside pilot projects exploring agri-voltaics in states like Andhra Pradesh and Karnataka, where crops flourish under strategically placed solar panels, demonstrate how India is envisioning a solar future and actively building it.

India’s rare earth strategy: Building resilience amid uncertainty

China’s sweeping export restrictions on rare earth magnets have triggered a global supply chain crisis, exposing the vulnerability of industries from electric vehicles to defense. For India, which relies heavily on Chinese imports for these critical materials, the move has served as a wake-up call. In response, India is accelerating a bold strategy to build a resilient, self-reliant rare earth ecosystem—ramping up domestic production, forging international partnerships, and offering new incentives to industry. As the world seeks alternatives to China’s near-monopoly, India’s rare earth corridor is emerging as a pivotal solution for both national security and global supply chain stability Image credit: Pexels Rare earth metals have become the latest flashpoint in global trade and technology. In April 2025, China, controlling about 60% of global rare earth mining and nearly 90% of refining—imposed sweeping export restrictions on rare earth magnets and key elements, sending shockwaves through supply chains worldwide. India, heavily reliant on these imports for its electric vehicles, electronics, wind turbines, and defense sectors, has responded with an ambitious, multi-pronged strategy to secure its future. China’s sweeping export restrictions on rare earth magnets have triggered a global supply chain crisis, exposing the vulnerability of industries from electric vehicles to defense. China’s Rare Earth Leverage China’s dominance in the rare earth sector is both economic and strategic. With state-backed subsidies and advanced processing capabilities, China produces over 60% of the world’s rare earth elements and refines more than 90% of global output. In April 2025, Beijing enacted export controls on seven critical rare earth elements and magnets, requiring exporters to obtain licenses for each shipment—procedures that are slow, opaque, and inconsistent across provinces. These measures were a direct response to escalating trade tensions and new tariffs imposed by the United States. By the early 2000s, China produced up to 97% of global rare earths. This dominance was achieved as Western nations shut down their own mines over cost and environmental concerns, while China invested heavily and perfected extraction and processing method. The impact is profound: global automakers, defense giants, and electronics manufacturers have warned of production delays and shutdowns, while some European auto plants have already halted operations due to supply shortages. China’s leverage extends beyond economics; by requiring end-user disclosures in export applications, Beijing gains deeper insight into global industrial ecosystems, further strengthening its strategic position. Even countries with significant rare earth reserves, like Australia, remain dependent on China for refining and processing. Effects on Key Sectors China’s export curbs have exposed vulnerabilities across India’s high-growth industries: Automotive: The EV sector, especially two-wheelers, faces acute shortages, with only about a month’s worth of rare earth magnet inventory left. Major manufacturers warn of production halts and price hikes if supplies remain disrupted. Defense: Rare earths like neodymium, dysprosium, and samarium are critical for missiles, radar, and advanced weaponry. The restrictions have heightened concerns about national security and the resilience of India’s defense supply chain. Electronics and Clean Energy: Smartphones, wind turbines, and green technologies depend on rare earth magnets. Disruptions threaten to slow India’s clean energy transition and digital infrastructure growth. Global ripple effects The immediate fallout has been acute. Automakers in Europe, the US, and Japan have warned of rising costs and production slowdowns. Defense industries, reliant on rare earth magnets for advanced weaponry, face strategic vulnerabilities. Even as China has begun to issue some new export licenses, the process remains slow and supplies scarce, keeping global manufacturers on edge. These disruptions have reignited calls for supply chain diversification. The US and EU are investing in alternative sources and recycling technologies, but the path to self-sufficiency is long and fraught with technical and environmental challenges Key developments in India’s rare earth corridor With the world’s third-largest rare earth reserves, India has long been seen as an underutilized player. That is changing rapidly in 2025. India’s strategy to break free from Chinese dominance is comprehensive: 1. Domestic Production Push : India is operationalizing its first major oxide-to-magnet plant in Hyderabad, set to produce 500 tonnes per year initially and scale up to 5,000 tonnes by 2030. Backed by government funding and India Rare Earths Ltd (IREL), the plant is expected to start production within six months. The government has also launched the National Critical Mineral Mission and is finalizing a ₹3,000 crore incentive scheme to boost domestic magnet manufacturing. 2. Resource Exploration and Development: The Geological Survey of India (GSI) has launched 195 exploration projects in 2024-25, including 35 in Rajasthan, to identify and fast-track new rare earth resources. New discoveries are being prioritized for commercial mining. 3. International Partnerships : India is building strategic alliances with Central Asian countries and exploring supply arrangements with Vietnam, the US, and others to secure alternative raw materials and reduce vulnerability to geopolitical shocks. 4. Policy and Industry Measures: The government is promoting private sector participation, R&D, and commercialization of magnet-making technologies. Production-linked incentives and subsidies are being considered to bridge the price gap with cheaper Chinese imports. While temporary arrangements to resume some imports from China are being discussed, the long-term focus is on building a resilient, self-reliant supply chain. Table: India’s Rare Earth Corridor Initiatives (Source: Media Reports) Challenges and the road ahead Despite holding the world’s third-largest rare earth reserves (about 6.9 million tonnes), India’s production capacity remains limited, ranking seventh globally, far behind China. Most domestic output has historically been allocated to atomic energy and defense, leaving other industries dependent on imports. The viability of Indian manufacturing is challenged by China’s aggressive price cuts, which saw India’s import value rise only 12% despite a 95% increase in quantity in FY25. Building a robust rare earth ecosystem will require: Sustained investment in mining and processing infrastructure Technological innovation and commercialization of new magnet-making methods Close cooperation between government, industry, and international partners China’s rare earth leverage has exposed the fragility of global supply chains and the risks of over-reliance on a single supplier. India’s rare earth corridor represents a decisive strategic response, combining immediate contingency measures, policy incentives, domestic capacity

India’s travel ad spend grew 28% in 2024, with 62% going to YouTube and Insta

YouTube and Instagram accounted for more than 62% of digital ad spending, driven by the popularity of short-form videos and influencer-led content that boosted campaign visibility. Influencer marketing saw a 45% year-on-year growth, with a strong focus on local travel, weekend escapes, and practical travel advice. Image credit: Pixabay India’s travel and tourism sector experienced a significant 28% rise in advertising expenditure in 2024, reflecting a strong rebound in consumer travel behavior and the sector’s renewed digital focus. This growth, detailed in a new report by Excellent Publicity in collaboration with TAM Media Research, is based on analysis of over 30,000 campaigns across platforms. As the industry adapts to post-pandemic consumer preferences, advertisers are increasingly prioritizing short-form, influencer-led content and targeting non-metro markets. Digital Dominance: 78% of Total Spend Digital advertising accounted for a commanding 78% of the total ad spend, marking a paradigm shift in how travel brands engage with audiences. This surge is attributed to rising domestic travel, a growing preference for quick, short getaways, and the increasing influence of social media in the travel decision-making process. Platforms like YouTube and Instagram led the charge, collectively absorbing over 62% of the total digital ad spend. Short-form videos, reels, and influencer collaborations dominated campaign formats. Influencer-led promotions grew by 45% year-on-year, underscoring the role of relatable personalities in driving travel inspiration and bookings. Campaigns frequently focused on practical travel tips, regional attractions, and spontaneous holiday ideas. A notable trend in 2024 was the shift from metro-centric to Bharat-centric advertising. Tier-II and Tier-III cities contributed 35% of total digital ad impressions, reflecting a strong surge in travel aspirations from smaller towns. Advertisers responded by embracing vernacular content, tapping into regional festivals, and offering cashback incentives to appeal to price-sensitive yet experience-hungry consumers. Travel brands customized content to local dialects and culture-specific themes, enhancing relatability and engagement. The increasing use of regional influencers further helped in bridging the trust gap between brands and local audiences. While digital leads the pack, traditional media retained its relevance in the advertising mix. Television made up 12% of total ad spending, particularly through regional entertainment and news channels. These were mainly leveraged during major holidays and high-audience events. Print media accounted for 3%, focusing on travel supplements, Sunday editions, and regional newspapers, especially during peak booking seasons. Out-of-home (OOH) advertising, including billboards at airports, bus terminals, and malls, claimed 6% of the ad budget, while radio received 1%, used mostly to amplify last-mile messaging during holidays and in heavy-traffic urban zones. Peak Seasons and Popular Destinations Advertising peaked in April to June, aligned with school summer vacations, and again between October and December, coinciding with festive travel and wedding tourism. Popular destinations featured in campaigns included Rishikesh, Ladakh, Udaipur, and international hotspots like Bali. Brands such as MakeMyTrip, EaseMyTrip, Club Mahindra, Agoda, Air India, and Thomas Cook were among the top spenders, together accounting for over 33% of digital ad spending. Their campaigns centered on holiday offers, interactive trip planning tools, and loyalty programs, designed to drive direct bookings and user engagement. Innovation and Emotional Storytelling on the Rise 2024 saw an uptick in experience-driven marketing, with a noticeable shift towards emotional storytelling and cultural exploration. Campaigns increasingly emphasized unique local experiences, wellness retreats, heritage tours, and eco-conscious getaways. Technological integration played a larger role, with AR/VR previews of destinations, voice-assisted itinerary planning, and AI-powered pricing tools becoming more mainstream. These tools helped travelers visualize and plan their holidays more effectively, enhancing engagement and conversion. Another noteworthy development was the rise of sustainability messaging. More campaigns incorporated themes such as responsible tourism, carbon footprint reduction, and support for local communities. This reflects growing consumer interest in mindful travel choices and aligns with global trends in eco-tourism The 2024 advertising boom in India’s travel and tourism sector highlights the sector’s agile adaptation to a changing consumer base and digital consumption habits. As travel becomes more democratized, with aspirations rising across the country’s socio-economic spectrum, brands are expected to double down on hyper-local personalization, mobile-first formats, and immersive experiences. Looking ahead, the momentum is likely to continue in 2025, with brands increasingly leveraging AI, data analytics, and creator economy platforms to fine-tune messaging and drive growth. With domestic and outbound travel both gaining traction, the next wave of advertising in India’s travel sector is set to be even more dynamic, inclusive, and digitally forward.

Fake on the plate: Is your food what it claims to be?

Food fraud is an increasing global threat with serious health and economic implications. Driven by profit, it involves counterfeiting, mislabeling, adulteration, and substitution—particularly targeting high-value foods like olive oil, seafood, honey, and spices. Advanced scientific methods such as DNA testing, spectroscopy, and IRMS, along with technologies like blockchain, AI-powered inspections, and smart packaging, are improving detection and supply chain transparency. In India, the FSSAI enforces food safety through the FSS Act (2006), supporting laws, and initiatives like Eat Right India. Yet, stronger global cooperation and tighter enforcement are crucial to closing regulatory gaps and combating cross-border food fraud effectively. Food safety is no longer the only pressing issue in the food and beverage industry—food fraud is emerging as a significant and growing threat. Frequently making headlines, it poses serious risks to both consumers and manufacturers. While not usually intended to cause harm, studies have shown that in areas with limited food security, such practices can contribute to under-nutrition. The occurrence of food fraud exposes critical gaps in the oversight and regulation of food supply chains. It also erodes public trust in food brands and regulatory authorities. Furthermore, once detected, food fraud often leads to costly repercussions for companies, including large-scale product recalls and damage to brand reputation. What is food fraud? Although there is no universally accepted definition, “food fraud” generally refers to instances where consumers are misled about the quantity, quality, or identity of the food they purchase or consume. Food fraud can take many forms, which may occur individually or in combination. These include– • Dilution: Mixing a high-value liquid ingredient with a cheaper liquid to reduce concentration and cut production costs. • Mislabeling: Providing false or misleading information on packaging or labels. • Unapproved Enhancement: Adding undeclared or unauthorized substances to a food product. • Substitution: Replacing a premium ingredient or component with one of lower quality or value. • Concealment: Intentionally hiding low-quality or defective ingredients within a product. • Counterfeiting: Illegally copying a brand name, design, recipe, or proprietary technique. Counterfeit risks consumer safety, as a fake product can contain unauthorized and hazardous ingredients. • Grey Market Production/Theft/Diversion: Selling unregistered, stolen, or diverted products through unauthorized channels. (Grey market foods are genuine products sold through unauthorized or unofficial channels. While not counterfeit, they are often priced lower than those in regulated markets, typically to bypass taxes, controls, or other official regulations. This type of trade is generally discouraged, as it can harm brand reputation and reduce profits. Diversion refers to the unauthorized distribution of products intended for specific markets—such as food designated for disaster relief or promotional events—being sold or used in unintended locations.) Most commonly faked food products Food fraud is a significant global issue, with certain products being more susceptible due to their high value, demand, and the complexity of their supply chains. The most commonly targeted food items include: • Olive Oil: Often diluted with cheaper oils like soybean or sunflower oil, and sometimes mislabeled regarding its origin or quality. • Seafood: Lower-value fish species are frequently mislabeled as more expensive varieties, deceiving consumers and affecting market prices. • Honey and Maple Syrup: These natural sweeteners are sometimes adulterated with sugar syrups to increase volume and reduce production costs. • Dairy Products: Milk and related products can be adulterated with substances like melamine to falsely enhance protein content, posing serious health risks. • Spices: High-value spices such as saffron, black pepper, and turmeric are prone to adulteration with inferior substances to increase weight or mimic color. • Fruit Juices: Expensive juices like pomegranate or blueberry are sometimes diluted with cheaper juices or water, misleading consumers about their purity. • Meat Products: Incidents like the horse meat scandal in Europe revealed the substitution of beef with cheaper horse meat in processed products. • Organic Foods: Non-organic products are occasionally mislabeled as organic to fetch higher prices, undermining consumer trust. • Coffee and Tea: These beverages can be adulterated with fillers or mislabeled regarding their quality or origin. • Wine: Counterfeit wines involve misrepresentation of origin, vintage, or grape variety, deceiving consumers. This adulteration compromises both the flavour and safety of wine. In some instances, counterfeit wine has been found to contain hazardous substances such as methanol, which can cause serious poisoning. Some of the most notable examples of food fraud across the world include: • Melamine in Milk (China, 2008): Over 300,000 people fell ill after milk and infant formula were adulterated with melamine to falsely inflate protein content (BCC, 2010). • Toxic Olive Oil Syndrome (Spain, 1981): Adulteration of olive oil with aniline-contaminated industrial oil caused around 300 immediate deaths and left many others with chronic illnesses (Gelpi, 2002). • Shrimp Injection: Injecting shrimp with gel or water to increase their size and weight, misleading consumers about product value. As per the FoodChain ID food fraud database data for 10 years (2015 – 2024) seafood, dairy, meat and beverages, were among the most frequently reported categories involved in food fraud incidents. Source: Food Authenticity Network (FAN) Top ten food commodities with the highest number of official food fraud reports in 2024 Source: Food Authenticity Network (FAN) The Impact of Food Fraud • Harm to Human Health: Food fraud can pose serious health risks to consumers. Toxic substances may be added, or essential nutrients removed, increasing the chance of foodborne illnesses. Additionally, undeclared ingredients can trigger allergic reactions or food intolerances, putting vulnerable consumers at greater risk. • Economic Harm: Fraudulently altered products are often of lower quality, meaning consumers pay more for less. This not only cheats customers but also harms genuine businesses that lose market share to dishonest competitors. Such fraud affects both luxury items like truffles and everyday goods like honey. • Harm to International Trade: The globalization of food production has made supply chains more complex and harder to monitor. With multiple stages and countries involved, controlling every point becomes challenging. This complexity increases the risk of fraud across ingredients, materials, and food products, undermining trust and integrity

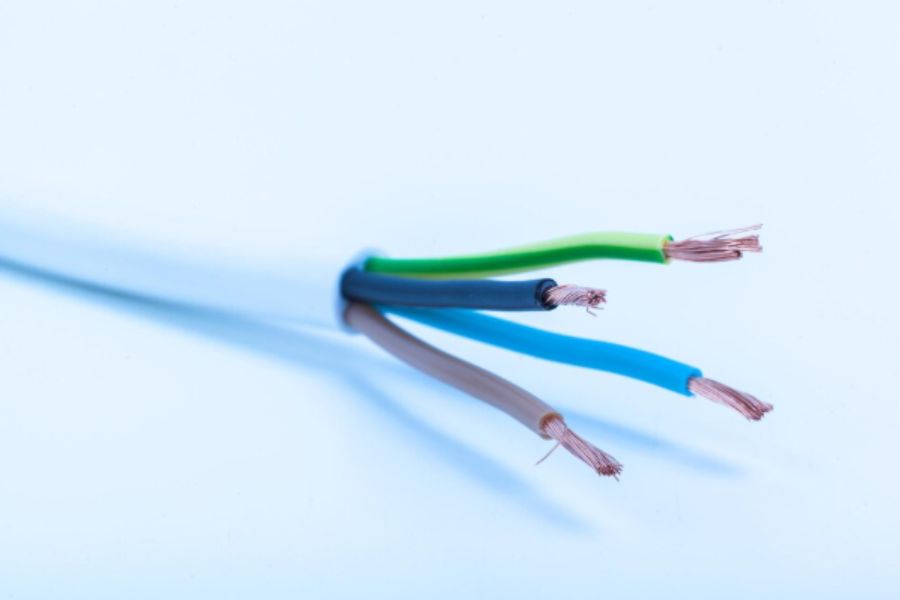

Insulated wires & cables: India’s growth and export potential

India’s wire and cable industry is poised for a transformative leap amid global shifts in energy, digital infrastructure, and connectivity. With robust growth across EVs, 5G, data centres, and renewable energy both domestically and globally—the demand for advanced, export-ready cable solutions is rising sharply. Backed by the fastest export growth among the top 20 countries and emerging opportunities in Africa, the Middle East, and post-conflict reconstruction zones, India has a rare chance to scale its global presence in HS Code 8544 products. This note outlines the opportunity landscape and product strategies that can power India’s ascent in this critical sector. Image credit: Freepik Due to the large-scale adoption of electric vehicles, 5G technologies, construction of data centres, and renewable energy expansion throughout the world, the global insulated wire and cable market size was valued at US$ 160.54 billion in 2019 and is projected to reach US$ 244.23 billion by 2027, registering a CAGR of 5.3%. India has a substantial opportunity to expand its export of cables. Under US Code 8544 — insulated (including enamelled or anodised) wire, cable (including coaxial cable) and others — India exported US$ 2 billion worth of products in 2024. It is currently ranked 20th globally, with China dominating the market at an 18% share. However, among the top 20 countries, India’s growth since 2020 has been the highest, at 100%. Wires and cables play an important role in sectors such as construction, telecommunications, power distribution, and automation. Of the total consumption, cables account for 80% of the market, while construction wires make up the remaining 20%. Taking advantage of expanding markets and current trade turmoil, India should aggressively explore avenues for increased sales in established markets and new regions in Africa and the Middle East. The data centre market in the Middle East and Africa (MEA) is experiencing significant growth, driven by increasing digitalisation, cloud adoption, and the development of smart cities. The market is projected to reach US$ 19.89 billion by 2030, growing at a CAGR of 14.93%. According to PwC, the Middle East is rapidly becoming a data centre powerhouse, with capacity in the region expected to triple from 1GW in 2025 to 3.3GW over the next five years. Data centres, fibre-optic broadband expansion, and telecom towers are set to become the new backbone of Africa’s economic growth, with South Africa, Nigeria, Kenya, and Morocco leading the charge. Mobile data consumption across Africa is expected to increase by 40% each year. Currently, there is 250MW of installed data centre capacity across Africa, forcing users to rely on facilities located thousands of miles away — often in South Africa or outside the continent. Demand for data centres across Africa is expected to exceed supply by 300% in the coming years. Off-grid solar installations are also growing rapidly in Africa. The sector provided 55% of new electricity connections in sub-Saharan Africa between 2020 and 2022, where over 80% of the unelectrified population resides. The World Bank Group has partnered with the African Development Bank to connect 300 million people to electricity across Africa over the next six years. The global 5G services market is projected to experience significant growth, with estimates ranging from around USD 250 billion by 2032 to over USD 4,564 billion by 2035. This expansion is being driven by increasing demand for high-speed connectivity, the deployment of advanced communication technologies, and growing adoption of 5G across various industries. The Indian wires and cables market is projected to grow significantly as well, supported by rising power demand, digital infrastructure development, and increasing EV adoption. A CAGR of 7.94% is expected between 2025 and 2032, potentially reaching a market size of USD 17.08 billion. There is also a likelihood of cessation of hostilities in Ukraine and Gaza in the near future. Whatever the terms for ending these conflicts, reconstruction will demand vast quantities of materials, including wires and cables. Ukraine’s reconstruction is estimated to cost $400 billion, while Gaza’s is projected at $25 billion. India should be ready to exploit these opportunities. To substantially increase India’s share in global markets, strategic product development should focus on high-growth niches, compliance with evolving global standards, and sustainability. Advanced Cables for Renewable Energy: Develop UV-resistant, high-temperature cables (up to 120°C) with low power loss for solar farms and offshore wind projects. Rodent-Resistant Insulation: Integrate materials like nylon or steel-braided layers to prevent damage in rural installations. Fiber Optic Innovations for 5G and AI Data Centers: Create high-density GPU-optimized fibers supporting 400–800 Gbps speeds for AI data centres, where GPU racks require 36x more fiber than traditional CPU setups. Introduce bend-insensitive fibers to improve rural 5G connectivity by reducing signal loss in tight-spaced telecom towers (only 40% fiberized in India vs. 85–90% in the US/China). Smart Grid and High-Voltage Transmission Cables: Develop ±800 kV HVDC cables to align with projects like KEC International’s ₹1,445 crore Power Grid Corporation orders. Embed IoT sensors in smart grid-ready cables for real-time monitoring of temperature and load fluctuations in smart cities. Cost-Competitive Alternatives to Copper: Develop aluminum conductor cables using AA-8000 series alloys for overhead power lines, reducing costs by 30–40% compared to copper. Use carbon fiber-reinforced composite core conductors to enhance strength and reduce sag in high-temperature environments. Export-Optimized Product Lines: Tailor products to EU (450/750V) and North American (600V) standards to capture 57% of India’s current exports (US, UK, Japan). Supply pre-terminated kits with plug-and-play optical fiber assemblies for data centres, reducing installation time by 50%. Invest in Nano-Composite Insulation: Improve dielectric strength and thermal stability for high-voltage applications. Global Certifications Secure UL (US), CE (EU), and GCC (Middle East) marks to counter Vietnam’s dominance (8.2M shipments) and China’s (5.8M shipments) in HS 8544. Indian SMEs should leverage PLI schemes to subsidize advanced manufacturing and forge partnerships with global players (e.g., Corning, Prysmian) for technology transfer. By prioritizing these innovations, India can target a 15–20% share of the $43B global fiber market and achieve 8–10% CAGR in HS 8544 exports by 2030. Suhayl Abidi, Research Advisor, Govt. of Gujarat

FY25 FMCG shift: Bigger baskets, rural driving growth

Indian FMCG trends in FY25 reveal a deeper shift beneath the surface of steady shopping patterns. While households maintained an average of 156 grocery trips, Kantar reports a marked increase in both basket size and value, highlighting a growing preference for larger and more premium packs. This evolving consumption underscores the dual realities of cautious consumer sentiment manifested in conservative trip frequencies and growing confidence, evidenced by heavier baskets and strategic brand choices. Image credit: Freepik A closer look at brand and regional performance reveals a clear divide. Unbranded products grew 6.1%, outpacing mainstream branded firms whose volumes increased around 3.6–3.9% . This indicates that many consumers especially in urban areas are opting for value options to cope with inflation and flat incomes. Rural India continues to provide the backbone for FMCG growth. As per Kantar, rural demand remains robust, while urban markets face pressure from higher costs and low wage gains. Sources like NielsenIQ and other analysts confirm that rural volume grew faster than urban, often by a large margin, driven by improved farm income, favorable monsoons, and expanding rural distribution networks. Branded firms such as Hindustan Unilever (+2%), Godrej (+4%), Tata Consumer (+6%), and Marico (+7%) showed modest growth in Q4 FY25. Meanwhile, smaller and regional companies recorded nearly 18% value growth, leveraging their lower cost base and rural reach . D2C and niche brands outside typical data ecosystems are also showing resilience, especially in targeted urban and premium segments. Wider Context & Market Implications A more detailed look reveals several layered nuances: Shrinkflation trends: Many brands are introducing smaller packs at ₹5–₹20 price points, which are gaining traction. This strategy supports entry-level consumption even as prices inch up . Premiumization persists: Despite financial stress, certain categories like bottled beverages, fabric softeners, personal care, and ready-to-eat foods continue to see heightened demand. Consumers are upgrading selectively, especially in urban markets Urban slowdown and strategic responses: Colgate-Palmolive highlighted a 2% drop in urban revenue, attributing it to financial stress faced by over two-thirds of urban consumers. Still, the company remains optimistic due to rural strength and digital marketing integration Looking ahead, industry players and analysts forecast a gradual recovery across urban India supported by softening inflation, better monsoon prospects, and possible tax reversals. Rural India is expected to continue fueling FMCG growth. Experts from Kantar, NielsenIQ, and economic research groups anticipate moderate gains for urban markets in the second half of FY26, while smaller brands will remain strong drivers in both markets FY25 has shown that how consumers shop is changing: trip patterns are unchanged, but baskets are bigger—stoking a cautious optimism in a difficult macroeconomic environment. While FMCG volumes have slowed overall, they remain buoyed by rural demand and lower-priced alternatives. The FMCG sector is bifurcating: urban consumers are cautious and price-conscious, turning to shrinkflated packs, unbranded items, and selective premium picks; rural India continues to exhibit strong growth, helping smaller and regional brands outperform. With inflation likely to ease and the rural economy staying strong, the coming months should see a steady recovery. FMCG players that can balance affordability with value especially in entry-level and rural segments will be best positioned to capture that upside.

India needs $2 Trillion to meet 2070 net-zero goal

India’s road to net-zero emissions by 2070 hinges on massive investments in clean energy, while still balancing economic growth and energy security. A new report by Moody’s and ICRA outlines the scale of investment needed—particularly in the power sector and highlights both the challenges and emerging opportunities across infrastructure, coal, renewables, ports, and data centers. India faces a significant challenge in achieving its 2070 net-zero emissions target, necessitating substantial investments, particularly in the power sector. According to a joint report by Moody’s Ratings and ICRA, the country will need to allocate approximately 2% of its real GDP annually over the next decade to the electricity value chain, which includes power generation, storage, transmission, and distribution. While renewable energy is set to play a pivotal role, India’s rapidly growing economy will continue to depend on coal in the short to medium term. The report projects a 32–35% increase in coal-based generation capacity, amounting to about 70–75 GW over the next 10 years. Simultaneously, an addition of approximately 450 GW in renewable capacity is planned. Abhishek Tyagi, a Moody’s Vice President and Senior Credit Officer, emphasized that solar and wind power will dominate new generation capacity additions over the next 20–25 years, with smaller contributions from nuclear and hydropower. He also noted that while the private sector is expected to remain active in India’s renewable energy sector, government-owned companies will increasingly play a significant role. Despite these ambitious plans, India’s renewable energy sector faces challenges. In 2024, renewables supplied only 24% of the country’s electricity, primarily due to integration and grid challenges. To meet the growing energy demand, which is projected to triple by 2050, India must expand its infrastructure and storage capabilities. In addition to the power sector, the report highlights a potential slowdown in road project execution in the near term, despite a healthy FY2026 budgetary outlay of Rs 2.72 trillion for the Ministry of Roads, Transport, and Highways (MoRTH). With road awarding projected to improve only in the second half of FY2026, revenue growth for road developers is likely to remain subdued over the next 12–15 months, as it typically takes 6–9 months from project awarding to on-ground execution. Conversely, ports and data centers are emerging as key growth areas. Under the Maritime India Vision 2030, the government has committed substantial capital expenditure to expand port capacity. ICRA anticipates a 3–5% increase in cargo volumes in FY2026, led by containerized cargo, petroleum products, and fertilizers, though global trade and tariff uncertainties pose risks. Overall, India’s path to achieving its net-zero target by 2070 will require a delicate balance between energy security, affordability, and the transition to cleaner sources. Substantial investments, supportive policies, and active participation from both the private and public sectors will be crucial in navigating this complex journey.