The pandemic and resulting economic crisis has had an immediate impact on edge computing deployments and has changed its future. To accelerate deployments, ensure extensibility, and drive efficiency and effectiveness, I&O leaders must create an edge computing strategy. Image source: Pixabay Edge computing is part of a distributed computing topology where information processing is located close to the edge, where things and people produce or consume that information. It is the epitome of Infrastructure-Led Disruption because it enables many new business outcomes. Infrastructure and Operations (I&O) leaders need to get in front of this trend, accelerating the enterprise’s efficient adoption of a growing range of edge computing use cases in order for the enterprise to be competitive. Edge computing projects are increasing, based on inquiry discussions. It is part of a distributed computing topology where information processing is located close to the edge (the physical location where things and people connect with the networked digital world). Often, edge computing projects are deployed independently, as custom solutions focused on a specific requirement, a specific use case or a specific part of the enterprise. However, enterprise experience has shown that edge computing projects multiply independently in different parts of the business, or expand from a single use case in a project to several use cases. Diversity in use cases is the norm in edge computing. But as the edge computing trend grows, synergy across projects and extensibility to enable new use cases is critical in overcoming challenges, creating standards, choosing technologies and managing costs. There are five important elements to an edge computing strategy, designed to simplify, synergize and systematize edge computing projects. Edge Computing Vision and Leadership The purpose of a vision is to provide an understandable target state that can help motivate and direct the team internally, and also that can be used to present measurable results to the enterprise. How will the organization operate differently with edge computing in five years? What new capabilities will be enabled? The edge computing strategy is linked to enterprise and technology strategies — what will they look like in five years? A vision for edge computing could include: An objective business impact, such as a percentage of digital business initiatives that include edge computing, net new business transactions enabled by edge computing, amount of money saved through edge computing initiatives, etc. Specific goals for edge computing use in the office, the factory, the store or branch. Percentage of customer interactions leveraging edge computing. Number of automation projects completed. Range of types of use cases deployed. Deployment agility, i.e., the number of POCs or time to deployment. Key to success of an edge computing strategy will be executive buy-in and sponsorship. For a strategy to be meaningful, there needs to be executive and staff support, and the vision needs to be well communicated. As the strategy changes — and an edge computing strategy will evolve as technologies and use cases emerge — updates to the strategy and vision also need to be well communicated. Identify Edge Computing Use Cases Edge computing use cases will be highly diverse, in diverse parts of the enterprise, with diverse objectives. An edge computing strategy should include an understanding of edge computing drivers, requirements and existing deployments. It should also have a process for proactively finding new use cases and correctly identifying use cases as they emerge. Identify the specific requirements that edge computing can address for the enterprise in the areas of latency, data, semi-autonomy and privacy. Identify existing technologies and deployments that should be included within the purview of the edge computing strategy. Identify potential use cases that could be addressed with edge computing, proactively and collaboratively with business units. Create a use-case clearinghouse to identify edge computing candidates as they emerge, with structured processes for how new use cases and edge workloads are identified, vetted and prioritized. Focus on Edge Computing Challenges Edge computing creates risks that need to be mitigated and new challenges that need to be overcome. An edge computing strategy needs to maintain a focus on them. Different industry verticals may have unique edge challenges, or risks that need to be mitigated. However, there are four challenges with edge computing that are applicable to the vast majority of enterprises – Distributed Computing; Security & Privacy; Distributed Data and Extensibility. Identify the risks, challenges and inhibitors that need to be overcome and mitigated and put special ongoing focus on those challenges in terms of management, investment and skills. Build and Communicate Edge Computing Standards Diversity is a defining characteristic of edge computing use cases, but that makes it even more important to find and maintain synergies by leveraging technologies, platforms, best practices, standards, processes and skills across disparate deployments. Many enterprises have a cloud center of excellence (CCOE). A CCOE is a centralized enterprise architecture function that leads and governs cloud computing adoption within an organization. The CCOE could be expanded to include edge computing, or a separate center of excellence could be created for edge computing. An edge computing strategy should include how best practices both outside the enterprise and from enterprise deployments will be captured and leveraged. Since edge computing is so diverse and so new, lessons learned will be extremely valuable to accelerate successful deployments and avoid duplicate efforts. The strategy should also include edge computing skills identification, development, roles and responsibilities, and organization and matrix organization structure. I&O leaders need to create an architecture function focused on edge computing (e.g., “edge center of excellence”). Build, maintain and communicate technology and architecture standards, frameworks and topologies that will be used across edge computing deployments. Capture and maintain best practices both outside the enterprise and from enterprise deployments. Identify and develop edge computing skills, roles and responsibilities, and organization structure. Ensure Success of Edge Computing Execution Because edge computing is an emerging concept where “firsts of a kind” predominate, enterprises will often be pioneering new technologies and new uses of technologies, and learning along the way. There are two unique aspects of edge computing that need to be considered in an edge computing strategy – Edge Computing POCs and Evolution Management Edge Computing POCs Edge computing

Mega Textile Parks should adopt complete integration

The Indian Government’s initiative to set up seven Mega Textile Parks across the country can help reinvigorate a sector employing millions of people and boost investments and exports. But the initiative needs to imbibe lessons from past experiences to ensure that these parks manage to provide the sector the leg up that it actually needs. The government in early October announced a Rs 4,445 crore scheme for setting up of seven mega textile parks in the next half a decade. Through introduction of cutting-edge technology, the parks can provide an opportunity on creating an integrated textiles value chain including spinning, weaving, processing and printing at a single location. The seven Mega Textiles Park are also expected to provide a spur to employment generation, with over 100,000 direct jobs and 200,000 indirect jobs in the coming years. However, the initiative should aim to address some of the concern areas like relatively small sizes of these parks and lack of complete end-to-end value chain integration. Image source: Shutterstock In a landmark move, the government in early October announced a Rs 4,445 crore scheme for setting up of seven mega textile parks in the next half a decade. The scheme aims to facilitate job creation in this labour-intensive sector, while also making it internationally competitive. As part of the new scheme, seven mega textile parks will be set up that would not only attract foreign direct investments but also introduce the much needed cutting-edge technology that will reduce manual labour and boost productivity. Through introduction of cutting-edge technology, the parks can provide an opportunity on creating an integrated textiles value chain including spinning, weaving, processing and printing at a single location. The government is inspired by the vision of 5F for achieving the envisaged targets: Farm-to-fibre Fibre-to-factory Factory-to-fashion Fashion-to-foreign. Scheme Details The Scheme for Integrated Textile Parks was launched in 2005 to provide industry with state-of-the-art world-class infrastructure facilities for setting up their textile units. For the scheme announced in 2021, the developer will need to develop and maintain the industrial park during the concession period. The Special Purpose Vehicle, with a major ownership of the state government, will entitle it to receive part of lease rental from the developed sites that can be used for expansion of textile industry, as well as providing skill development initiatives. For setting up a greenfield textile park, the Indian government will provide capital support of up to 30% of the project cost, subject to a maximum of Rs 500 crore. On the other hand, the maximum amount will be capped at Rs 200 crore for brownfield sites. To ensure quicker set up of an industrial estate, the state government can provide up to 1,000 acres of land. There is also a provision of using 10% of the park’s area for Commercial Development such as shops, offices, Hotels and Convention Centres. The Parks will be developed in a Public Private Partnership based Master model on Design-Build-Finance-Operate-Transfer format and will be located at sites having strength for textile industry to flourish with the requisite linkages. The Ministry of Textiles confirmed that a number of states have already shown interest in moving ahead with the scheme. This includes not just includes leaders in apparels like Tamil Nadu and Gujarat but also other states such as Odisha, Andhra Pradesh, Rajasthan, Assam, Karnataka, Madhya Pradesh, Telangana and Punjab. Furthermore, the parks are envisaged to help India achieve the United Nations Sustainable Development Goal 9 – Build resilient infrastructure, promote sustainable industrialization and foster innovation. The seven Mega Textiles Park are also expected to provide a spur to employment generation, with over 100,000 direct jobs and 200,000 indirect jobs in the coming years. India’s Textile Industry-Overview & Potential China, United States, Vietnam, Bangladesh and India have the lion’s share of the global textiles and apparel markets. Some key statistics are given below: In 2018, China accounted for almost half of the global textile production and a third of the total exports Bangladesh is second largest individual country for apparel manufacturing and textile business contributes to 80% of its exports Vietnam’s industry has grown by 17% annually since last five years, now accounts for 16% value in the country’s GDP. Its exports to more than 150 countries demonstrate the popularity of its garments From time immemorial, India’s textiles industry has been a global leader. Currently, the country is the 6th largest exporter of apparels and textiles in the world. The share of the domestic industry is less than 5% of the GDP, little over 12% of its export earnings and 7% of the industry output. Despite the textile and apparel industry being 2nd largest employer in India, with direct employment to over 45 million people and totally to 100 million people in allied industry, the overall output is quite low. Besides being a powerhouse of cotton and jute production globally, India is also a leader in hand-woven fabrics and 2nd largest silk producer. The Indian textiles market is growing at a CAGR of 10% since 2015-16, demonstrating a consistent performance. However, demand uptick and augmenting e-commerce avenues are expected to result in a robust CAGR for the next few years. India’s resilience in the textiles sector was tested during the heights of the Coronavirus pandemic in 2020, being an importer of the PPE kit, used extensively in medical premises. However, the country quickly adapted to the changing times and has become the second-largest manufacturer of PPE globally, with over 600 companies certified to produce PPEs today. The global market worth of just this segment is expected to be over US$ 92.5 billion by 2025, up from US$ 52.7 billion in 2019. The Textile Park scheme is amongst a slew of measures taken by the government that will facilitate the industry’s growth in the coming years. Some of the key projections include: Industry size will become US$ 190 billion by 2025-26 from US$ 103.4 billion in 2020-21. Explosion of retail markets, providing a thrust to organised retail surging to 40% of total sales by

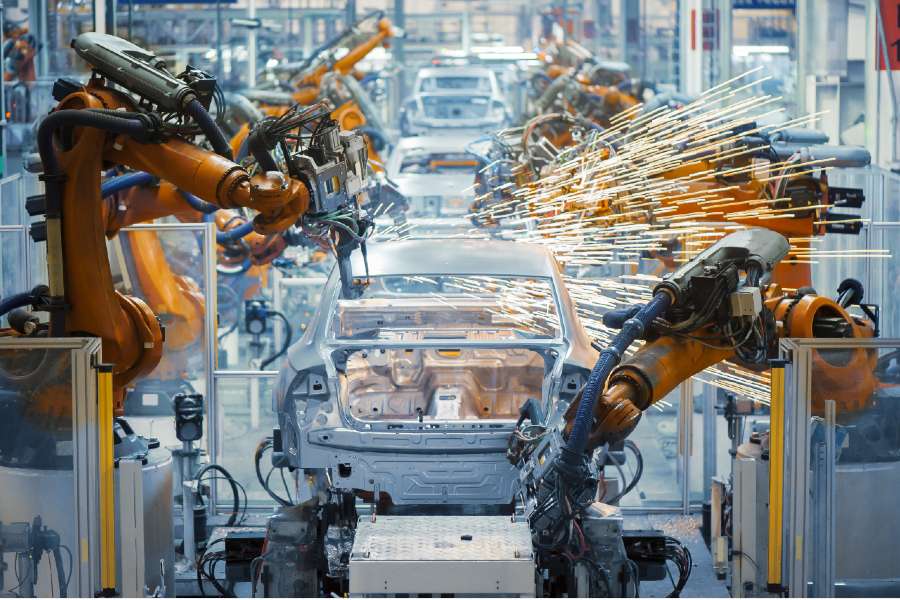

Auto Industry: Identifying the path of least resistance

As the auto industry struggles to recover from the effects of the pandemic, it needs to also define its future direction in context of the shift towards emission friendly fuels and technologies. Stakeholder consultations need to focus on how this transition can be as smooth as possible for the Indian industry. The auto industry in India, with an investment of about Rs 8.3 lakh crore, is one of the largest contributors to the economy as well as employment. However, the industry was one of the worst hit by the slowdown in the economy. It was already going through a tough phase even before the COVID pandemic, growing at a negative CAGR of 1.9% during 2016-21. As the sector scripts its post-pandemic recovery, it faces multiple challenges like fuel prices, high taxation, shortage of semiconductors and the shifting priorities towards EVs. Government-industry consultations have to focus on smoothly managing this transition. The auto industry in India, with an investment of about Rs 8.3 lakh crore, is one of the largest contributors to the economy as well as employment. Over 3 crore people are directly or indirectly associated with the sector. The industry currently contributes 7% to India’s GDP and 49% to its manufacturing GDP. It manufactured 22.6 mn vehicles including Passenger Vehicles, Commercial Vehicles, Three Wheelers, Two Wheelers, and quadricycles as of April-March 2021, while exporting 4.1 million units. Notably, India has a distinctive positioning in the heavy vehicles arena, as it is the largest tractor manufacturer, second-largest bus manufacturer, and third largest heavy trucks manufacturer in the world. The Indian automobile market is the world’s fourth in terms of vehicle sales. Many reputed multinational automobile companies have understood the potential of the Indian auto market and invested heavily in the automobile industry, making it one of the key drivers of economic growth and enabling India to emerge as one of the top investment destinations. The automobile industry was one of the worst hit by the slowdown in the economy, as it was already going through a tough phase even before the COVID pandemic. According to Society of Indian Automobile Manufacturers (SIAM), the current Indian automobile industry CAGR is in negative. The CAGR recorded in 2011-16 was 5.7%, which dropped to -1.9% during 2016-21. More so, sales of vehicles dropped by 32% since 2020. A large number of skilled and semi-skilled workers have lost their jobs in automobile industry and its allied sectors, as many factories have closed down. This has a spin-off effect on related sectors such as ‘iron mining’, steel, medium and small manufactures of vehicle accessories & parts, service stations, dealerships, etc. Apart from the COVID pandemic, there are host of other factors, which indeed are big setbacks to the already struggling auto sector. The industry is asking for relief measures, including on various taxes and cess levied by the government to bring down on-road prices of vehicles. Challenges Rising fuel prices not only hurt consumers, but also haunt governments. Personal vehicle users have to spend more on buying fuel that destabilizes their household budget. In turn, they have to reduce their spending on other products. Consumers voluntarily or involuntarily move towards the public transport system, and increase in ridership can cause the transport system to collapse. However, rising fuel price provides an opportunity for the automobile sector to work on more fuel-efficient vehicles or better alternatives. Hybrid and electric vehicles are the results of continuous R&D to reduce the dependence on fuel. Fuel price in India depends on crude base price, freight charges, excise duty, dealer commission, VAT on dealers’ commission, etc. Currently, fuel price in India is the highest in the world when measured in terms of purchasing power parity. There has been a 74% increase in excise duty. India is one of the largest manufacturers of tractors and the second largest two-wheelers and fifth largest car manufacturers in the world. GST Rate on automobiles in India is at 18% to 28% plus Cess ranging from 1% to 15% on two-wheelers and luxury level cars. Further, there is an additional 22% cess if vehicle exceeds certain body & engine size specifications. Besides the pandemic, disparity of GST has flattened the two struggling segments of the automobile industry – two-wheelers (80% market share) and passenger vehicles (14% market share). To improve safety and reduce carbon emissions, regulators implemented numerous norms of safety and environmental regulations. While upgrading safety features and emission norms from BS-IV to BS-VI are important for safety of consumers and the environment, it has led to a steep hike in the cost of vehicles as automakers are forced to invest heavily in their production line. The industry has spent a lot of money in upgrading cars to BS-VI norms from BS-IV. Third Party Insurance cover is now mandatory. The clause of upfront payment for 3 and 5 years in the Insurance policy (for cars and bikes respectively) is not going down well among consumers, as they are always reluctant to pay overhead expenses. The crisis of Non-Banking Financial Companies (NBFCs) is another concern for the auto sector. The demand for cars and two wheelers has fallen drastically by nearly 20%. Overall sales of automobiles for 2020-21 are forecasted to be lower than the units sold in 2015. Besides, the six-month moratorium on repayment announced by RBI is constraining liquidity in the market. In the current festive season, auto sales have posted the most disappointing performance in a decade, declining by 18% YoY. While the demand was healthy, automakers have been unable to meet it due to the shortage of chips and supply disruption in semiconductors. The government has announced the PLI Scheme with incentives worth Rs 26,058 crore for auto sector, auto components and drones. This is require investments of at least Rs 1,000 crore by existing players and Rs 2,000 crore by new players in these sectors over the next five years. Support of the government will not only boost the industry, but also give a new life to the medium and

In agriculture, storage is power

Prasanna Rao, CEO & Co-Founder, Arya, discusses how startups in the post-harvest agri-tech space are building a complete suite of services to the farmer, encompassing tech-enabled quality grading, aggregation, storage, swift and smooth digitally-enabled financing, and a marketplace on one platform one platform. For any industry in any economy to prosper, finance is the necessary fuel to sow green shoots of growth, the Indian agrarian sector being no different. Credit is tight and working capital is low, from start to finish in the Indian agricultural economy. In most cases, the humble Indian farmer doesn’t have enough money to use Storage-as-a-Service, and is thus forced to sell to traders to generate cash flow at harvest when prices are lowest. The trading segment is itself fragmented (unlike the West where a few juggernauts handle the bulk of the volume) and is therefore comprised of a spectrum of small to large traders who progressively handle different parts of the supply chain – from buying from the farmer and giving him immediate cashflow to themselves selling to larger traders who have more capital and can therefore aggregate more. Time is always money, but additionally in agriculture, storage is power. Post-harvest – the more time that elapses, the more prices usually tend to appreciate past that harvest supply push. And to wait it out and capture that price increase, you need to be able to access cheap storage to tuck it away. To be able to store without being starved for cash flow, you need credit. He who has capital generates more capital, and in Indian agriculture, that isn’t the farmer. World over, we have seen a shift in this trend – as farmers this century have grown wealthier (due to greater control over their own storage), a subtle but powerful shift has occurred in the dynamics of global agri value chains, as more value has accrued to the producer. Arya and other Indian agri-techs are working to bring this shift to India. They are creating opportunities for smallholder farmers and FPOs at the fringes of inclusion. The ability to finance farmers cheaply and instantly is in the first place driven by the right asset footprint. Unlike a vast majority of Warehousing Service Providers, new age agritechs are primarily geared towards the farmgate – 90% of Arya’s footprint is, for example, in primary and secondary agri-centers, wherein over 40% of our borrowers are using formal lending sources for the first time. This enables farmers and FPOs to simultaneously access storage and financing very conveniently, and allows them to participate in the price appreciation post-harvest. In many cases, post-harvest agritechs are the only lenders present in these areas. At the time of harvest, the farmer will bring his/her produce to a warehouse for storage, at which point in time, quality is first assessed using a combination of regular processes as well as AI-enabled techniques. Once the produce is graded and stored, the farmer receives a digital balance, which can then be used for borrowing. Warehouse receipt finance has become a viable and easy solution to the needs of small holders. Many banks/NBFCs insist on a formal credit history before lending. Moreover, agri-tech lenders issue small ticket loans which many bigger lenders will not. By lending only against secured collateral which it controls, a fintech like Aryadhan doesn’t require credit history for lending. This is key to unlocking financing demands in near farmgate markets. Onboarding and borrowing processes are simple and intuitive and sanctioning of a loan to a farmer is done in less than 5 minutes. For a loan, one needs only basic Aadhar KYC, which can be scanned and uploaded digitally. For reference, banks and other bigger NBFCs typically take a week to 10 days for this stage as they don’t have the physical presence in the immediate vicinity. Sending someone to a rural village in India and processing a loan could typically take at least a week. Speed here is of the essence and agri-techs like Arya enable swift borrowing for clients. Very importantly, the rates at which agri-techs lend are much lower than competing lenders in these areas, making it a win-win for the farmer as well the agri-tech company. To close this particular loop, the final key service is a marketplace, so farmers or FPOs can sell their produce through a digital platform instead of having to search for a buyer themselves. With a wider footprint, a digital platform is able to connect a wider circle of buyers and sellers than an average participant today typically transacts with, thereby increasing the chances that the seller finds the best price on the platform. Once the commodities are sold through the platform, the loan gets closed automatically. The balance of the proceeds are refunded to the buyer immediately, thereby reducing friction and increasing convenience as well as utility significantly for the farmer. Arya’s model agri chain is a very good example of how agrtitech maximises every value of the grain that travels through the value chain to benefit smallholders with better returns. Thus, startups in the post-harvest agri-tech space are building a complete suite of services to the farmer, encompassing tech-enabled quality grading, aggregation, storage, swift and smooth digitally-enabled financing, and a marketplace to capture the best price for the goods all on one platform, thus enabling profitability for the farmer and a much-needed shift in value in the chain towards the producer.

Drone PLI: A flight towards self-reliance

Given its strength in innovation, information technology, prudent engineering, and huge domestic demand, India has bright prospects to be a global drone hub by 2030. A combination of the right policies such as the recent drone PLI scheme as well as industry efforts such as foreign collaboration will be the secret ingredients in India’s journey to success. Commonly known as unmanned aerial vehicles (UAVs), ‘drones’ operate without any human presence but are controlled with human involvement. They can be deployed in various sectors such as agriculture, mining, infrastructure, surveillance, emergency response, transportation, geo-spatial mapping, defense, and law enforcement. Recently, these UAVs have garnered a lot of interest because the government announced new liberalized Drone Rules, 2021, and the drone PLI scheme to support the development of the drone sector. According to the government estimates, the annual sales turnover of the drone manufacturing industry is poised to grow from Rs 60 crore in 2020-21 fold to over Rs 900 crore in FY 2023-24. The drone manufacturing industry is likely to generate over 10,000 direct jobs over the next three years. A combination of the right policies such as the recent drone PLI scheme as well as industry efforts such as foreign collaboration will be the secret ingredients in India’s journey to success. Image credit: Pexels Commonly known as unmanned aerial vehicles (UAVs), ‘drones’ operate without any human presence but are controlled with human involvement. Though they were envisaged for aerospace and military activities, drones have made their way into myriad uses due to the effectiveness and security they bring. Thus, they can be deployed in various sectors such as agriculture, mining, infrastructure, surveillance, emergency response, transportation, geo-spatial mapping, defense, and law enforcement. Recently, these UAVs have garnered a lot of interest because the government announced new liberalized Drone Rules, 2021 to support the development of the drone sector. The liberalised rules, which have reduced the number of forms to be filled from 25 to just 5, will also provide a thrust to the growth of medium and small enterprises, which are at a nascent stage of growth. Since the fee for remote pilot licenses has been reduced and the validity of license being ten years, it can translate into a phenomenal growth opportunity for the startup ecosystem to thrive in this sector. The new rules facilitate security clearance for operating and flying tiny drones in air. In addition, the increasing focus on cargo deliveries will be driven through drone corridors. The government has also augmented the payload from 300 kg to 500 kg. While the MSMEs engaging in drone manufacturing need to demonstrate annual turnover of Rs 2 crore, drone component makers will need to show turnover of Rs 50 lakh, encouraging investment from companies to invest in the flourishing ecosystem. Towards this end, it also introduced the drone PLI scheme. The drone PLI scheme has an outlay of Rs 120 crore spread over three financial years. An incentive of 20% will be offered on the value addition made by a manufacturer of drones and drone components for all 3 years. The government envisages that India can be a global drone hub by 2030. This is attributed to the country’s strength in innovation, information technology, frugal engineering and its huge domestic demand. Commenting on the scheme, the Ministry of Civil Aviation stated: “The drones and drone components manufacturing industry may see an investment of over Rs 5,000 crore over the next three years. The annual sales turnover of the drone manufacturing industry may grow from Rs 60 crore in 2020-21 fold to over Rs 900 crore in FY 2023-24. The drone manufacturing industry is expected to generate over 10,000 direct jobs over the next three years.” The drone PLI Scheme will ensure component and drone manufacturers come to India, leveraging the advantageous manufacturing environment. Furthermore, it will allure investor foray and hence is a vital step for achieving India’s vision of an Aatmanirbhar Bharat. The scheme can make India a drone hub by 2030 and make it at par with the other global giants such as US, China and Israel amongst others. It includes a wide variety of drone components: Airframe, propulsion systems (engine and electric), power systems, batteries and related components, launch and recovery systems; Inertial Measurement Unit, Inertial Navigation System, flight control module, ground control station, and associated parts; Communications systems (radio frequency, transponders, satellite-based etc.) Cameras, sensors, spraying systems and related payload etc.; ‘Detect and Avoid’ system, emergency recovery system, trackers etc. and other components important for safety and security. The UAV sector & its tremendous growth potential The Global Drone Market was about US$ 18.28 billion in 2020, which is expected to surge to US$ 40.9 billion by 2027, witnessing a compounded annual growth rate of 12.27%. The US is the largest drone market globally and accounts for 50% of the drone investments. It is estimated that by 2024, US commercial drone unit sales will be four times vis-à-vis 2018. The west Asian country Israel continues to be a global force in the multibillion-dollar UAV industry. The country commenced experimenting with drones back in 1969 and a study by business consulting firm Frost and Sullivan in 2018 highlighted that it exported a staggering US$ 4.6 billion worth of UAVs, constituting 10% of the country’s military exports. India, which is fast expanding the use of drones, also signed a deal with Israel, that would not just contribute to Israel’s exports but also facilitate access to advanced technology. While the military segment continues to command over 56.7% of the Global Drone Market in 2020, the increased use of drones for diverse elements is expected to push up demand from other segments in future. According to research reports, North America will continue to dominate the drone market. However, Asia-Pacific will be the fastest-growing market. For example, the Chinese drone market is catching up quickly, with about 558 thousand registered drone operators in 2020. India, too, is gearing up to be a force to be reckoned with the global UAV sector.

Sustainability in seafood industry

Dr. Sunil Mohamed observes that since the concept of sustainability can no longer be separated from the seafood industry, the Indian marine sector is gearing up for this challenge to establish its hold in global seafood exports. Image credit: istockphotos The Food and Agriculture Organization states that between one-third and 40% of all fish produced is now traded internationally. This makes fish and fisheries products one of the most traded food commodities in the world. A careful analysis of data suggests that global average consumption of fish and other seafood has grown from 9.9 kg in the 1960s to 20.5 kilogram in 2019. 10 countries with the highest per capita consumption of fish and seafood include Iceland (91.19 kg), the Maldives (84.58 kg), Portugal (57.19 kg), South Korea (57.05 kg), Japan (46.06 kg), Spain (42.4 kg), China (38.49 kg), France (34.24 kg), Italy (29.82 kg) and Australia (26.12 kg). India’s per capita consumption of fish and seafood is at 6.76 kg. Further, China has been a major player in this trade in 2020. Some of the other major aquatic products exporting countries are Norway, Vietnam, Chile and India. Of late, countries like Vietnam are importing raw fish, adding value to it and then re-exporting these value added seafood products. The Indian seafood industry: Time to cast a wider net Looking at India, specifically, the nation has the advantage of having a large exclusive economic zone of 2 million square kilometres. Accounting for 7.96% of the total global fish production, India is the second-largest fish and aquaculture-producing country. The country’s seafood industry contributes about 1.24% to the country’s GVA and supports the livelihood of over 28 million people in India. The total marine exports increased from US$ 3.5 billion in 2011-12 to US$ 5.9 billion in 2020-21 as per MPEDA. This trade is buoyed by rising demand in the US and Europe. It suggests that of late, Southeast Asia has also emerged as an important destination for India’s marine exports. There has also been a commodity-wise change in India’s exports. For example, India’s shrimp exports have risen from a share of 30% in 1990s to 74% in 2020-21. Increase in shrimp exports have been majorly due to the rise in aquaculture. The other commodities of marine exports are frozen fish, frozen cuttle fish, frozen squid, dried items, live fish and chilled items. It is also interesting to note that while the US is the top destination for Indian seafood exports in value terms (US$ 2.45 billion), the Southeast Asian region was one of the top export destinations in 2020-21 in terms of volume (2177 MT). This implies that India is trying to diversify its seafood exports in terms of both the products offered and the markets to which they are exported. Source: MPEDA (All units are in US$ mn) 5-year trend of India’s marine exports Product Value exported in 2017-18 Value exported in 2018-19 Value exported in 2019-20 Value exported in 2019-20 Value exported in 2020-21 Frozen shrimp 3,726.38 4,848.19 4,610.59 4,889.12 4,426.19 Frozen fish 672.47 733.17 699.09 513.6 402.31 Frozen cuttle fish 292.73 369.88 282.29 286.4 221.97 Frozen squid 388.64 385.01 359.71 314.23 273.37 Dried items 199.77 163.53 189.58 140.81 156.94 Live items 61.05 45.41 55.89 46.43 32.72 Chilled items 116.02 101.78 89.2 90.34 65.14 Others 320.54 434.58 442.16 397.77 378.3 Total 5,777.61 7,081.55 6,728.5 6,678.69 5,956.93 Source: MPEDA (All units are in US$ mn) Seafood industry & the question of sustainability Today, the importance of utilizing fisheries and aquaculture resources responsibly is widely recognized as several fish stocks started collapsing globally in the late ’80s. Almost 90% of global marine fish stocks are now fully exploited or overfished owing to rising populations, higher incomes, and greater awareness of seafood’s health benefits. According to the data computed by the World Bank, the situation is worst in low-income and middle-income countries, where weak regulation and enforcement have produced above-average declines in fish stocks. It notes that illegal fishing constitutes 20% of the global catch. This situation needs to change as fisheries are crucial to global food security and nutrition. This is where the question of sustainability becomes crucial for the industry. Sustainable fishing is crucial to ensuring sustainable fish stocks, minimizing environmental impact and allowing effective fisheries management by preventing illegal fishing and cutting out destructive fishing practices. In this context, eco-labelling is increasingly being adopted to maintain the productivity and economic value of fisheries, while providing incentives for improved fisheries management and the conservation of marine biodiversity. According to the FAO: Eco-labels are seals of approval given to products that are deemed to have fewer impacts on the environment than functionally or competitively similar products. The rationale for basic labelling information at the point of sale is that it links fisheries products to their production process. Product claims associated with eco-labelling aim at tapping the growing public demand for environmentally preferable products. In India, the Marine Stewardship Council’s (MSC) ‘Blue Label Certification’, certifies that their fishery uses sustainable methods of fishing. A fishery in Ashtamudi lake has obtained this certification. Such an endeavor can boost India’s share of seafood export, which is currently 4% of the global trade. Sustainability is also linked to traceability. Overseas consumers and processers want to know the source of the product. For example, the EU is demanding catch certificates, in which fishers declare where they caught the fish processors that carry that label export markets. This calls for investment by the Indian seafood sector in the transition to sustainable fisheries. So, India, too, has started embracing this change, since a number of other countries have started demanding this proof. The government has designed Pradhan Mantri Matsya Sampada Yojana (PMMSY) for promoting sustainability and traceability from ‘catch to consumer’ In addition, the government has also introduced initiatives to promote various new techniques for both fresh water and saline water species. For example, RAS is a highly intensive, eco-friendly and water-efficient farming system that can be encouraged for small-scale fish farmers and entrepreneurs to initiate and

With Digital economy, a new course for competition law

The explored, and yet unexplored digital technologies of the present era open gateways into greater forms of data harvesting and control, as well as providing creative opportunities for its monetization. This has also fuelled the rise of unfair competitive practices in the digital realm, which need to be managed with a radical and highly dynamic approach. Today, a number of anti-competitive practices are governing the digital landscape. These refer to acts and omissions violating ethical business norms by putting the consumer at a disadvantage. This could be by collusion and/or restricting the trade of businesses working on an equivalent plane and/or restricting the trade of businesses working in a different industry but remain relevant to the operations of the predatory organization. In an online space, a networking platform may have justification for certain practices due to the complex balancing act they conduct between parties. This complexity, combined with the many parties and people involved with those parties makes current competition measuring tools such as price testing and market share, redundant. As the yet unexplored technologies of the future open gateways into greater forms of data harvesting and control, as well as providing creative opportunities for its monetization, regulatory frameworks have to dynamically evolve to keep this activity in check. Image source: Shutterstock Competition law has existed since the Romans sought to regulate the corn trade. With the advent of modern economics, as propounded by Adam Smith, the market became the all-encompassing force that pervaded lives. Companies rose in stature and size by taking advantage of the early capitalist rat race and devising ways to monopolize the market, some even going to the extent of employing unfair means. Today, the same unfair means, albeit in a different form, are being utilized to capture a greater number of consumers through a different, less regulated medium – the digital space. A calls for increasing regulation On the back of severe quarantines around the globe, consumers settled into the new normal of relying on apps and contactless services for even the most mundane tasks. Brick-and-mortar giants such as Walmart and Target made aggressive strides into the e-commerce space. This speaks volumes about the growing consumer reliance on the digital economy. The recent changes in legislation in South Korea and Australia, have reignited debate about the scope of competition law and its limitations in dealing with the digital space. Previously, it was considered that the present antitrust framework and its provisions suffice for the control of dominant organizations, but perspectives around this have changed. Some primary concerns with competition in the digital realm include: The increased opportunities for economies of scale and scope. Difficulty in determining the extent of digital influence as compared to physical influence. The complexity of algorithms that are not fully comprehended. The uphill task in relation to consumer data protection. Global response South Korea’s amended Telecommunications Business Act will bar app market operators from forcing certain payment systems on mobile app development companies. This was in response to the onerous, and arbitrary terms and conditions that govern the Apple App Store in particular. Similarly, the Australian Government asked the ACCC to develop a mandatory code of conduct to address bargaining power imbalances between Australian news media businesses and digital platforms, specifically Google and Facebook. Regulators cannot afford to be unconcerned about compliance with regard to the above differences between the physical and digital space. The above four primary concerns add a layer of difficulty to the challenge of crafting an anti-trust framework that reels in internet giants. In regard to the first concern, the digital world, not restricted by tangible realities, holds greater potential for upscaling and expansion. This certainly offers opportunities to budding companies, but on the flipside, has seen an unbridled increase in the market share of existing titans. As mentioned before, traditionally brick-and-mortar entities such as Walmart and Target have made forays into e-commerce. Their dominance as retailers, coupled with large investments in advertising their online ventures, has resulted in their consumer base simply shifting to their phones to purchase from the same shops. The small semblance of an opportunity for growing retailers that presented itself at the start of the pandemic, seems to be largely compromised. In regard to the second concern, the digital space being vast and open, it is hard to determine the exact influence of powerful companies. Dominant internet and application-based businesses are typically multi-sided, i.e., they serve as networking platforms between two or more parties. General constraints imposed by these platforms affect all these parties and the degree to which they can be considered unfair towards them can determine the quantum of penalty. However, in an online space, a networking platform may have justification for certain practices due to the complex balancing act they conduct between parties. This complexity, combined with the many parties and people involved with those parties makes current competition measuring tools such as price testing and market share, redundant. In regard to the third concern, algorithms curating content today form a huge part of public opinion and behaviour. There is a lack of understanding about these lines of code as they use data from varied sources and the exact process followed to interpret such data is not open to scrutiny. Given this fact, it is not inconceivable that these algorithms can be manipulated to the advantage of their makers. The argument that suspicions cast on these lines of code is unwarranted is a specious one for if one were to presume that the algorithms work as presented, it still limits consumption of content to simply a few organizations, considering the fact that the curator sitting behind the screens assorts and recommends content on the basis of the quantity of clicks. The vicious cycle continues – one click leads to more and more clicks, thereby leading consumers to be encapsulated within the sphere of just a few corporations, completely unbeknownst to us. In regard to the fourth concern, India has taken admirable steps to safeguard consumer data, by

Green hydrogen economy: Towards a resilient future

Dr. J.P. Gupta opines that India’s drive to green energy transition by embracing green hydrogen is a key to a future-proof economy. He adds that the development of this industry is mainly dependent on the production, storage, and transport technologies identified in many sectors with lessons to be gained from LNG export. However, funding will be critical to developing the green hydrogen value chain in the country. Decarbonization of the global economy holds several benefits, as it is getting increasingly obvious that all crises are interlinked and we need to deal with them holistically. Recent studies have reflected upon the rising public concerns with regard to the climate crisis and the increasing need to address the knowledge gap around the rising global temperatures, which have a global impact, including infectious diseases like the coronavirus. There will be a huge thrust given to net zero-emission by the world’s top carbon emitters – the US and China. What is going to happen, consequently, is that it will accelerate the decarbonization of the world. That creates a tremendous opportunity for clean energy players to up their game. Green hydrogen, particularly, is one technology that is being conceived the world over as a pathbreaker in driving an economy towards net-zero carbon emissions. India, too, has started treading on this pathway to decarbonize development. Any pathway assumes a proactive policy role in creating incentives that would encourage the private sector to co-invest (with the government) in building the green hydrogen economy, infrastructure and supply chain. The time is now ripe for implementing hydrogen as a key part of the energy system in the country. India’s ambition to look at green energy transition as a part of holistic societal development is promising. A mission-driven economy is a future-proof economy. Hydrogen Technologies Hydrogen can be an ideal green fuel, considering it is the universe’s most abundant element. Hydrogen energy is extremely adaptable, as it may be utilized as a gas or a liquid, transformed into fuel, power or heat, and produced in a variety of ways. Natural gas, coal, and oil are now the primary sources of energy for industrial operations, accounting for over 20% of world emissions. The industry must enhance energy efficiency in order to reduce emissions. Hydrogen produced from electrolysis using renewable-driven energy sources, such as solar or wind, is known as ‘green hydrogen’. The rapidly declining cost of renewable has been a motivation for the growing interest in green hydrogen. Hydrogen is a new and viable alternative to fossil fuels, with a well-established market and a full value chain in place. The core components of hydrogen technology are readily available for scaling up the hydrogen industry. This is critical to reducing costs to build green hydrogen economy. Electrolyzers and fuel cells have been in active use for a century. In Norway, Nel Hydrogen (formerly Norsk Hydro) had the world’s most significant hydrogen production as early as 1927. Norway is, thus, one of the pioneers in the development of essential components in hydrogen production and the handling of hydrogen. In recent years, Fuel Cell technology has started to become competitive in price, e.g. conventional engines running on fossil fuels. For water electrolysis, learning effects and economies of scale will result in CAPEX cost reductions of 60% in the Net Zero Emissions by 2030 compared to 2020. Production cost reductions hinge on lowering the cost of low-carbon electricity, as electricity accounts for 50-85% of total production costs, depending on the electricity source and region. Hydrogen Storage Hydrogen’s energy content by volume is low. One kilogram of hydrogen takes about 11 m3 at ambient temperature and atmospheric pressure. Consequently, for storing hydrogen gas, it needs the reduction of a large volume requiring high pressures, low temperatures or chemical processes. Hydrogen gas or liquid can be stored physically. Physical state methods constitute compressed (high-pressure), liquid (cryogenic), and cryo-compressed tanks. Alternatively, materials can be used for storing hydrogen as well. This process consists of either chemical storage (absorption within the material) or physisorption (absorption on the material surface). Chemical storage includes materials such as ammonia (NH3), metal hydrides, formic acid, carbohydrates, synthetic hydrocarbons, and liquid organic hydrogen carriers (LOHC), while porous materials like carbon, zeolites, complex hydrides, metal/ covalent organic frameworks do so by absorption processes. Priority industrial applications Storage becomes important when one looks at a very important application of hydrogen – transportation. Transportation and distribution of hydrogen is a very important step in the use and implementation of the hydrogen economy. Transportation of hydrogen can be done in its gas or liquid form. Hydrogen gas can be transported via pipelines like natural gas, by high-pressure tube trailers where compressed hydrogen transporting can be done by trucks, railcars and ships. In its liquid state, hydrogen can also be transported by trucks and ships in cryogenic tanks. Transporting primary energy like ethanol, methanol, biomass, LOHC, ammonia or solid hydrogen storage is another alternative to produce hydrogen at the point of use. At present, in India, the fertilizer industry consumes a large amount of natural gas. This is used to produce ammonia, the central intermediary for providing nitrogen in all nitrogen-containing fertilizers. Significant changes are required to reduce emissions from the ammonia production process further. This could be made possible by ensuring that the hydrogen feedstock used for fertilizers is produced using renewable electricity to manufacture green hydrogen (green ammonia). Methanol is readily available across emerging and developed markets, making it attractive for locations with no/less hydrogen infrastructure and safety capabilities. It is currently primarily produced from natural gas, and its two-stage process requires hydrogen production. The average plant produces 5,000 tonnes per day, at a yearly hydrogen consumption of 266,104 tonnes. Key industrial players include Methanex and Sabic. In India, methanol is imported and is generally produced from a carbon source. Refining is the most immediate source of potential industrial demand for green hydrogen. A typical annual requirement of hydrogen at a refinery might range from 7,200 tonnes to 108,800 tonnes. This requirement can increase up to 288,000

PLI scheme for textiles: Weaving the fibers of growth

India’s textile and apparel sector is a key contributor to its GDP growth, employment and export basket. Yet it has lost its global competitiveness, leading to a dip in exports. Will the recently introduced textile PLI scheme finally help the industry weave threads of growth in the international market? The Indian textile sector is one of the largest industries in the world & the second largest contributor to employment generation in India. It is also a key contributor to India’s export basket, accounting for roughly 12% of total India’s export earnings. The sector has a lot of potential in terms of growth and development. A push in the right direction will enable further growth prospects in the sector. The Production Linked Incentive (PLI) scheme has recognized the key gaps in the textile industry, by covering man-made fibers (MMFs) and technical textiles in its ambit. It seeks to enhance India’s manufacturing capabilities by attracting investors and boosting exports. While the scheme can help ramp up production and build larger scale players, improving exports would also need effective redressal of issues like environmental clearances, low technology intensity, skill gap and high import content to truly leverage the advantages of PLI in global export growth. Source: Pexels Valued at US$ 75 billion in 2020-21, the Indian textile sector is one of the largest industries in the world. It is a key contributor to India’s export basket, accounting for roughly 12% of total India’s export earnings and the second largest contributor to employment generation in India. Yet the industry lags behind competitors like China, Bangladesh, Germany and Vietnam in the international market leading to a dip in textile exports. India’s textile and apparel exports have increased at a CAGR of 5% since 2005-06, amounting to US$ 33.5 billion in 2019-20. India’s share in global textiles and apparel exports has declined from 4.84% in 2015 to 4.34% in 2018. The pandemic worsened the situation, as India’s textile & apparel exports are expected to fall around 15% to reach US$ 28.4 billion in 2020-21. Tuho boost the sector’s export performance, the government, therefore, recently cleared a Rs 10,683-crore production-linked incentive (PLI) scheme under for man-made fibre and technical textile products. The scheme is also likely to generate employment opportunities for 1 crore people over the next 5 years. Commenting on the scheme, Commerce and Industry Minister Piyush Goyal said: We hope that this decision will produce some global champions. Factories based around aspirational districts or Tier-3 & Tier-4 cities will be given priority. It will especially benefit Gujarat, UP, Maharashtra, Tamil Nadu, Punjab, Andhra Pradesh, Telangana etc. Product coverage The PLI scheme is expected to cover nearly 40 product categories under the MMFs and 10 product categories in the technical textile segment. It will offer incentives of Rs 7,000 crore for man-made fibre (MMF) apparel, and Rs 4,000 crore for technical textiles. The MMF category covers garment segments like trousers, shirts, and jerseys of man-made fibers, whereas technical textile category includes products like bandages, adhesive dressings, safety airbags, and diapers. The complete product categories are defined under the various chapters of the CUSTOMS TARIFF ACT, 1975. India’s share of exports for these aforesaid categories and products is significantly less in the global market. Moreover, India is also lagging behind in the man-made fibres (MMFs) textile trade due to the high cost of raw materials, higher tariff barriers, and cheaper imports from the neighboring countries. The graph given below depicts the top 10 exporters of textiles and how India is lagging significantly behind its neighbours. MMFs and technical textile segments have much stronger competitors across the globe, whereas in India, these products are not manufactured to the full potential. The scheme seeks to establish few large world-class global companies in technical textile and MMF segments that have the potential to grow. They can develop in terms of both – size and scale, by the adoption of cutting-edge technology and thereby penetrate global value chains. PLI Scheme – Eligibility and Incentives The policy also seeks to attract fresh investments to the tune of Rs 19,000 crore in firms manufacturing textiles locally. It also hopes to increase the turnover of the textile industry by a whopping Rs 3 lakh crore over five years. To make India into a global textile manufacturing hub in the next 5 years, PLI Scheme incentives worth Rs 10,683 crore would be provided to both greenfield and brownfield investments. Incentives under this scheme would vary with the product categories in the range of (~3% to 11%) of the incremental marginal revenues year-on-year for the five-year period. An individual or a firm ready to invest a minimum of Rs 300 crore to manufacture MMF fabrics or technical textiles will be eligible to apply for incentives under the first phase of the scheme, while an individual or a firm willing to invest a minimum of 100 crores will receive benefits in the second phase of the scheme. The following are the industry’s requirements and asks to make the scheme more efficient and effective: Reducing the limit for new greenfield investments: Indian textile sector is more fragmented as compared to many other sectors, as there are very few companies in Indian textile sector which have potential of manufacturing garments, unlike in neighbouring countries like China and even Bangladesh. Every process in garment manufacturing is being done by the multiple players, and for each process there are multiple layers. Moreover, the textile industry in India tends towards labour-intensive techniques, and thus it can achieve the benefit of the policy in real terms, the investments limit should have to be kept at the minimum. Special allocation to MSME sector: The textile sector in India is largely driven by MSMEs and the scheme enables medium scale units to operate at larger scale, as such units get larger benefits in terms of investment inflows enabled by the PLI scheme. A harbinger of good times? Since the traditional and conventional textile sector of India has reached a level of saturation in terms of innovation, value-addition and

Shree Gajanan Industries: Competitive entrepreneurship, good ethics and transparency

Hiten Bhimani, CEO, Shree Gajanan Industries explains how the success of the company is attributed to unfailing commitment to quality and constant innovation, like the first-of-its-kind technology in the non-Basmati segment in the country. The company is now catering to highly quality-conscious markets like the US, Australia, Japan and Europe and is working on expanding its export markets. IBT: How would you describe the journey of Shree Gajanan Industries, its vision, and key achievements? Hiten Bhimani: From being a pioneer, Shree Gajanan Industries has come a long way to be a leading firm in the rice processing industry today with an annual turnover of around Rs. 200 crores. Our journey had a humble beginning in Nizamabad (then Andhra Pradesh, now Telangana), when it all started in a compact shack in the year 1949. It was later established as a brand in 1969. Gajanan aspires to expand its global presence, guided by the ideals of the late Kanji Bhai, the fountainhead of the company. His principles in life are inherited by each member of the team — honesty, integrity, perseverance, and commitment. Thus, the company believes that sustainability lies in competitive entrepreneurship, good ethics and transparency that flourish on right values and not profits. One of the key achievements is that Gajanan is amongst the few brands promoting SRI method of paddy cultivation. In SRI paddy cultivation, the seed requirement comes down by 80 %, the water requirement is reduced by 50% and the yield is also much better. IBT: What were some of the challenges that the company faced during this time? Hiten Bhimani: In the year 2008, the first shock came in the form of the export of rice being banned. That was when we realized that a lot of standards need to be put in place so that this brand survives for the next 100 years. Over the next few years, energies were channelized towards this and finally, in 2012, we got the ISO 22000 certification, and then in 2014, the FSSC 22000 certification. In 2016, the brand got organically certified, while in 2017, we got the GSFI certification. Subsequently in 2018, we got the SEDEX Smeta for our ethical and social compliance practices. Gajanan was also a part of an MOU between the Chinese customs and the Indian Agricultural department for phyto sanitary certification. IBT: What is your company’s reach as per product segments and markets? What are the key ingredients for success in international markets in your view? Hiten Bhimani: Shree Gajanan Industries is into processing indigenous rice varieties and is now moving from rice commodities to the entire range of groceries such as dals, masala & spice powder, pickles and other value additions. The idea is to bring the products right from the farm to your table. Currently, the company is catering to highly quality-conscious markets like the US, Australia, Japan and Europe and is working on expanding its export markets. IBT: What are the key ingredients for your success in international markets, which could be imbibed by other Indian companies? Hiten Bhimani: We look for long-term partnerships. Transparency and ethics have played a key role in our success in the international market. Moreover, the brand has focused on its unfailing commitment to quality and constant innovation like the first-of-its-kind technology in the non-Basmati segment in the country. This helped it to not only become a household name in the country for different varieties of rice, but also to establish its footprint around the globe. IBT: What key lessons has Shree Gajanan Industries learned from the COVID-19 pandemic? How have you adapted and realigned your business model? Hiten Bhimani: The core lesson learned from the COVID-19 pandemic is how to manage disruption. When things are uncertain, we need to be innovative and have solutions for problems. Since we were in essential commodities; our supply chain was not majorly affected, but the international supply chain did get affected due to logistics. IBT: What advice would you like to offer to young entrepreneurs on managing risk, coping with failure, and leadership? Hiten Bhimani: Focus is important on key parameters and building one’s strengths. Failures are milestones to success and teach us many things. Leadership is the single most important thing to focus on in a moment of crisis. One should come forward to take decisions in such moments. IBT: How do you view India’s level of competitiveness in your sector, and how can it be enhanced? Hiten Bhimani: Our sector largely depends on the agricultural policies in India. It’s been monitored and governed under MSP. So, there’s very little that we can do to compete in the international market as the cost is largely dependent on the MSP. This interview is a part of TPCI’s Connect initiative.